Major tailwinds:

Lengthening of life expectancy because of advance in medical science

Coming of age of millennials forming families

Headwinds:

I see usual cyclical ones. Are there any structural ones?

I noted larger built-in square footage houses of my rental SFH appreciate higher in percentage term and much easier to rent out… not sure whether this is a secular trend… if it is… then would push up demand of building materials and require larger lot, hence the higher cost of building and higher price/sqft of land… higher price for existing houses.

Some observations from a couple of my tenants.

This is in one of my month to month rental units in the bay area. (I have time sensitive termination clauses that are in my favor.)

First tenant - Software engineer couple who went back to their home country during covid (and truly worked remote! joy!). Came back and rented from me and within a couple of months bought a house in the bay area. They did complain about the increase in house prices but that didn’t stop them from buying.

Second tenant - Also software engineer - also went remote during covid. They also want to buy a house in the next 2 months.

Seems to be a weird desire to own even with prices on a tear - maybe it’s all to do with that secular uptrend.

Reference your article that you linked, only millennials effect is structural. The other two is cyclical. The third one (WFH) is unclear… need to monitor… The uptrend is for everywhere not just suburb and exurbs, for the urban2

Notice the two structural reasons in OP has nothing to do with Covid-19.

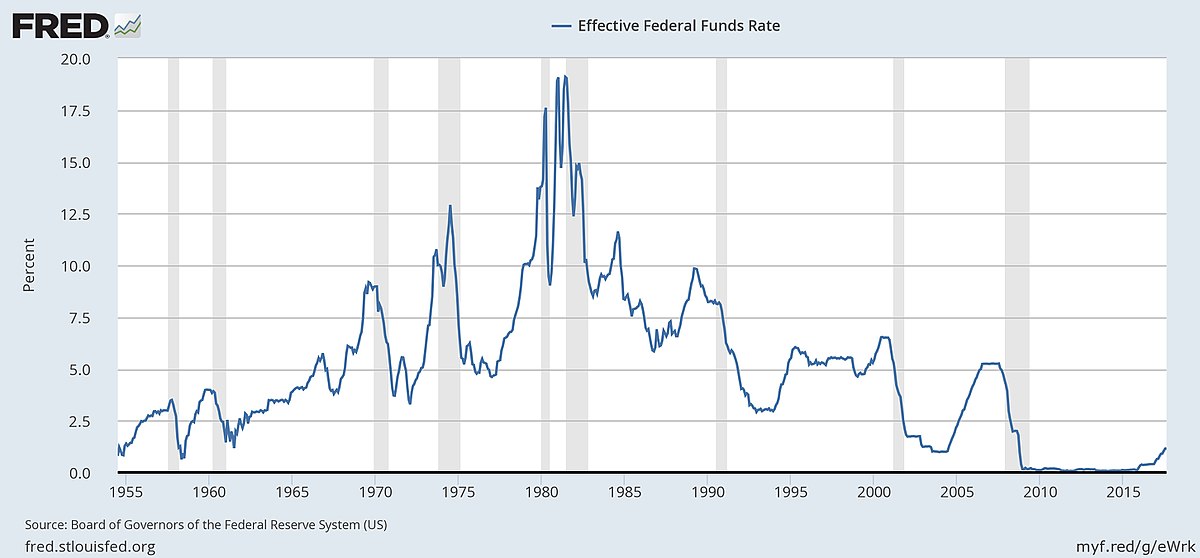

Effort is on to justify endless money printing. Therefore, the interest rate will only reflect the cost of handling money (not the cost of borrowing the money itself - because with MMT/QE/Printing/, the additional money comes with no cost to printer. The real cost is paid by the lenders and savers. That is why money printing is transfer of money from savers to spenders ). So, home prices will rise and fall a the rate additional money is printed (or destroyed if that is an option in MMT).

So next time housing market takes a dive down, just print more, it will come back up.

That is the past. Going forward? Next 10-20 years? If not sure, then is not a headwind nor a tailwind.

That is interest rate per se is not a major factor. Need a more precise metric. Otherwise, should be considered as a non headwind or non tailwind. Frankly, is unclear whether interest rate is a driving up demand or reduce demand or how does it affect supply.

I did not understand your comment. But, what I am saying is that in the last 50 years or so, the society has been made to believe that unlimited money printing does no harm to anyone. Which is wrong obviously. Savers are hurt by money printing. Assets have to be repriced every time new money is created. The benefit people receive whose dollar amount is fixed loose value (like life insurance). If home prices rise without any real demand, it is nothing but repricing to reflect the devalued currency.

This thread is about figuring out the long term (structural) headwinds and tailwinds. Other aspects and short-term headwinds/tailwinds are not relevant to the OP.

Is there any reason for the trend to change? Government at all levels would be screwed if rates increase too much. When the existing bonds mature, they won’t be able to afford interest payments on new ones.

I know this line of reasoning. So you are cocksure it won’t change? I know the past trend and the reason for it, but I am not sure about the future trend…