If it is foolish for you to sell, why would be wise for someone else to sell?

Singular goal of the FED is to stop inflation – balance supply and demand so that you don’t have a crazy “increase” in prices. There will be a slow down and stabilization happening. 50% decrease needs something more – like a huge layoffs in tech. Not happening.

Folks are going to hold and ride out. There will be some unfortunate forced sells that may be up for grab for some discount – you can already see these kind of deals.

It’s foolish to think you are special and that others will sell and you won’t have to. I don’t think there will at lot of sellers. In fact inventory is historically low. And there arestill too many buyers including you and me and everyone else on this forum.

Here you go . Only $3.2m in South Padre Island Texas.

$3.2m. It would have to drop 90% to get my bid. But the agent is a hoot…

I think it’s Stiflers mom.

Homeowners wearing the ‘golden handcuffs’ of low mortgage costs are reluctant to sell their homes now that rates are much higher

Homeowners with low mortgage rates are balking at the prospect of selling their homes to borrow at much higher rates for their next homes, a development that could limit the supply of houses for sale for years to come.

Housing inventory has risen from record lows earlier this year as more homes sit on the market longer. But the number of newly listed homes in the four weeks ended Sept. 11 fell 19% year-over-year, according to real-estate brokerageRedfin Corp. That is an indication that sellers who don’t need to sell are staying on the sidelines, economists say.

Because SFH in Bay Area are cash flow negative money pits. I have all big MFHs, no SFH.

SFH will be decimated as they are worse than Bitcoin. At least Bitcoin doesn’t burn cash every month.

Your thesis would require at least a majority of SFH to be a rental with negative cash flow. If you think that, then you’re showing how little you know.

The vast majority of SFH are owner occupied. If owners sell, they have to live somewhere else. That means paying high rents or a mortgage rate over 6% to buy a different home. It’s better to stay in a home with a mortgage rate under 3%.

How many sales over the last few years were to landlords? Most haven’t been adding new rentals. They bought their rentals 5+ years ago at much lower prices. They are cash flow positive with zero reason to sell.

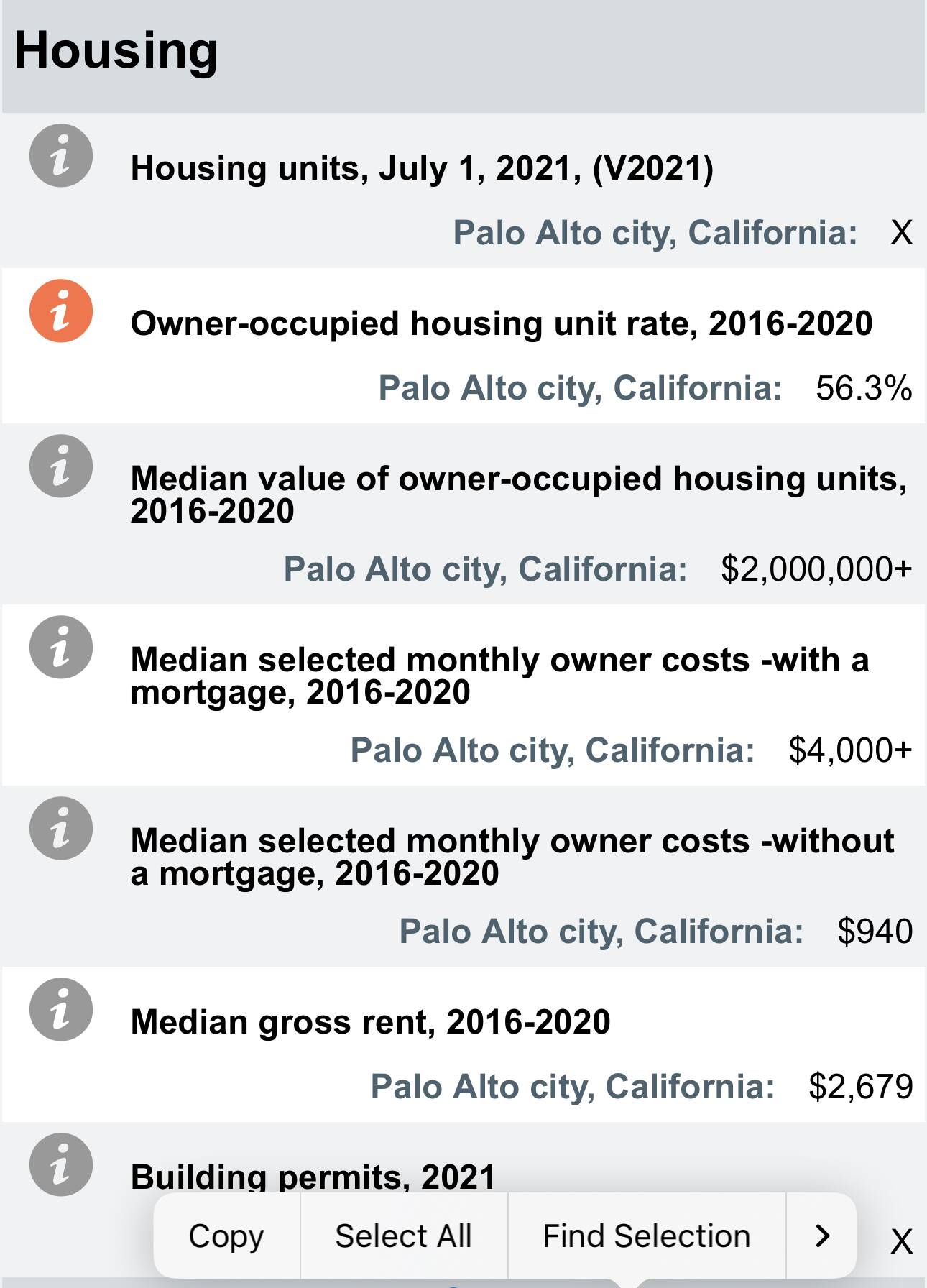

This is certainly a fallacy. In PA at least 30-40% of housing stock seems to be on rental market. In fact more than half of the recent sales I have seen were put on rental market right after sale. I hear same for MP, LA. Don’t know about tier 2 towns. But with Bay Area exodus and remote work I expect pretty high share of investment SFH there too.

30-40% rentals in PA? pure speculation bullshit. No data. I doubt it’s a hotbed of rental RE. Look at Craigslist… how many listed fir rent? Vacancy rates? 20? houses for rent in a city with 20 k homes… extreme housing shortage… like everywhere else

Data we need data points without which you state with bias like your 50% crash from peak !

In fact recent sales I have seen were put on rental market right after sale => There are many reasons for it, that is not show case for 50% crash, neither 20% crash.

To me @Elt1@Jil@marcus335@acre@spacehopper either are old perma deniers, the kinds who thought smartphones will never replace keyboard phone, digital camera will never replace film and streaming will never replace blockbuster, or are not prepared to handle 50% RE price crash. I suggest if you guys want to prosper smart up and don’t fight Fundamentals and Fed.

10 yr tr up 6% today and Fed is not even half way done and inflation is still rising. Good luck guys.

Also someone said stocks won’t cross June lows. Well S&P is within 100 points of June bottom. Haha.

Let’s look at this mathematically. Stock market down about 25% and mortgage rates up about 3%

That changes Bay Area 2.2 million dollar house total payment from $10000 to $15000 per month for someone who was going to put 20% down (now 15%).

So all else being equal, this same person who could afford 2.2 million dollar home can now afford 1.6 million dollar home.

That’s a 28% house price decline.

But that’s for buyers putting down smaller down payments, many in real BA have more cash to put down larger down payment and therefore less affected by mortgage rate changes.

At the same time, that doesn’t consider that supply will likely be reduced a little bit.

Those 2 latter factors mean it is unlikely housing prices decline a full 28% at current market status. Perhaps 15%. (I think we are already down 10% from peak).

To even think about 30%, we would have to have a further massive decline in the stock market.

That’s unlikely, and 50% just isn’t feasible under even many Black Swan events.