I love to give people a hard time. Specially when the lack of manners come to play.

Tonight, it was a prosperous night, the best in 30 years, a solar guy introduced me to 2 clients. Both are 39-45 yo. I got to roll over a $208K from a 401K into an annuity to avoid the 10% penalty, from there will do an immediate withdrawal of $40K per year to put into an IUL, so the taxes won’t increase their tax bracket. Then, open 4 IULs for their wives and sisters, 2 Worker’s comp audits from a chain of restaurants and furniture stores. Same 2 clients for the 10% tax deduction from gross income. Then an audit of both cost segregation, plus credits on hiring employees, plus deferring capital gains for 30 years on a property being sold for $3.5M. Then, solar panels, and energy saving programs for both businesses. Reduction of credit cards fees, there’s more as we discover their incomes and needs. Not bad for about $125K in commissions.

I think I will retire after these deals.

But, here I am, I lost track of the importance of numbers, I was discussing a $6K a year contribution, it is petty stuff. Not worth anybody’s nor my time. WTH was I thinking?

I just wish good luck seeing the present crash of the stock market, about 1,500+ points lost in a few days, I hope you get a prosperous return in your investment. You will need the best of lucks, really!

I gave you above the scenarios of how to prepare for the retirement so your SS check doesn’t get taxed.

Use it or lose it.

Because I was busy working and didn’t pay attention at all. Yes, I boo about able to hold despite the deep 50-99% decline, the secret is I wasn’t looking at the account Also, Apple has a good team. TSLA seems like an one-man show, Elon doesn’t let any1 shine.

With AAPL too, Steve Jobs was single man show!

Same with AMZN

FB, Mark Z, single man show

Everywhere the case is there.

It is all founders they provide their life to bring up the company, not an easy task.

The truth is comfort of the investor. Each one of fixated with some companies and believe blindly.

Understanding good company at early time is essential and buy and hold like WQJ is exceptional no matter whether stocks go up or not.

One day, I talked a friend, when he was a fresher/newbie investing, asked him to choose best company for buy and hold.

Believe it or not, he is holding NFLX since $80, but only 4 stocks.

Somehow I do not get that mindset even with S&P500!

Apple is not one-show during SJ. Jony is well known. So is Tim, Peter, Jon, Tony, Scott, Avie, etc.

FB has two personalities, Mark and Sheryl.

AMZN is kind of like TSLA, other than Jeff, everybody are relatively obscure.

Learn to play Chess You would realize making moves that have no impact can be a powerful move.

It is because of this impending recession, I am skeptical and trading back and forth to increase my cash position.

I still regret, last year, losing 167k even though I clearly noticed a downfall in Sep 24th, but never knew how depth the fall would be ! Experience, experience and experience matters a lot…

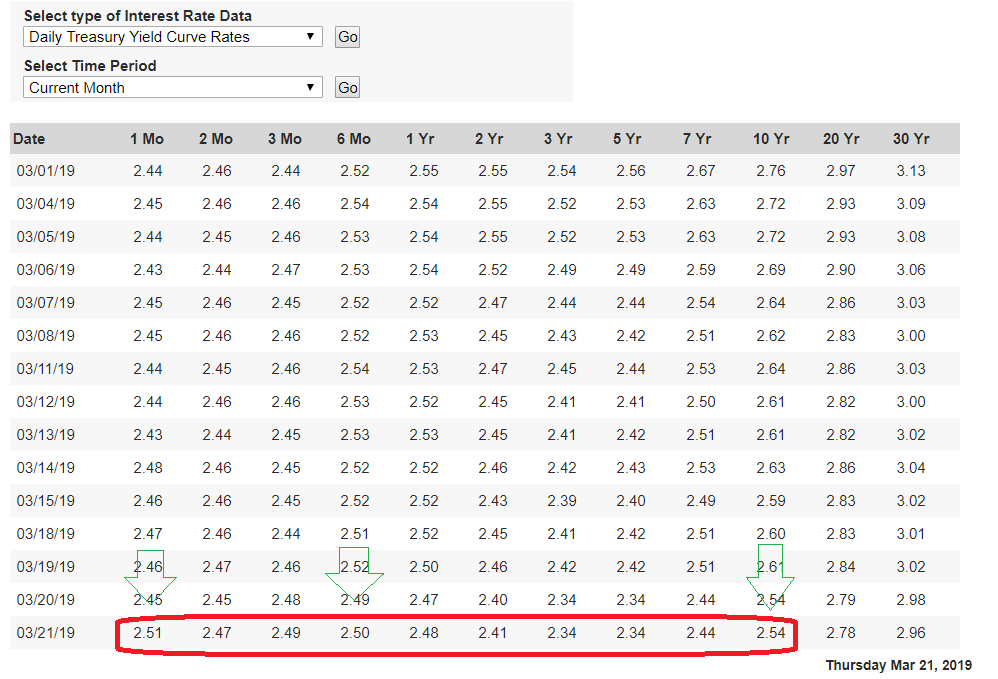

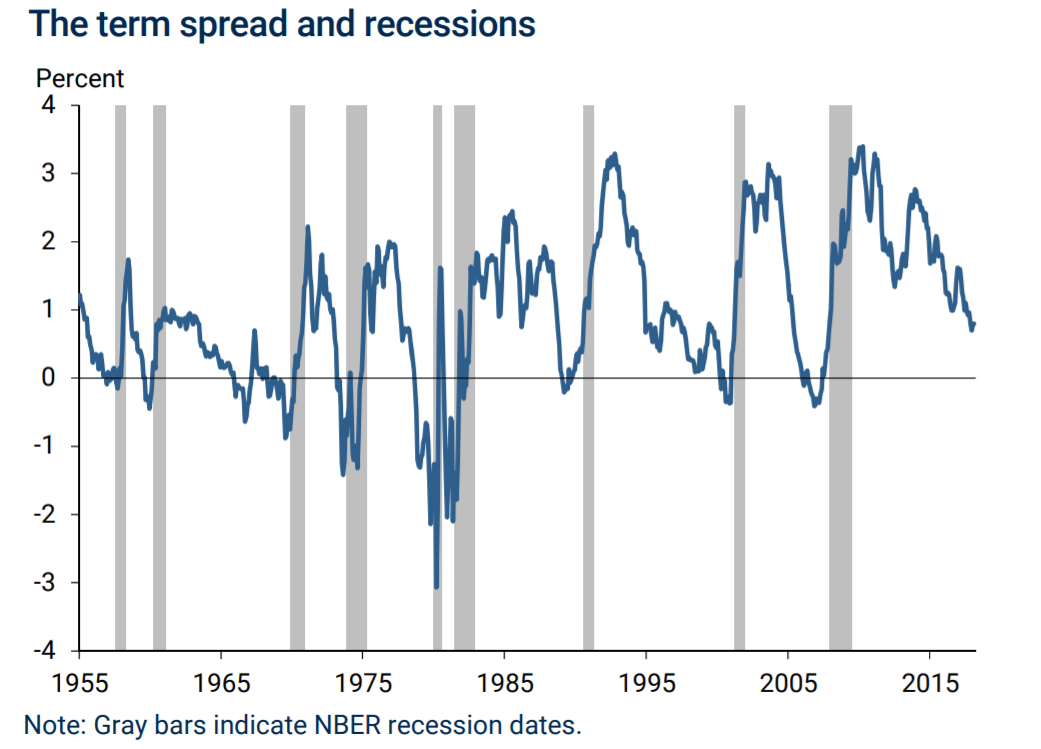

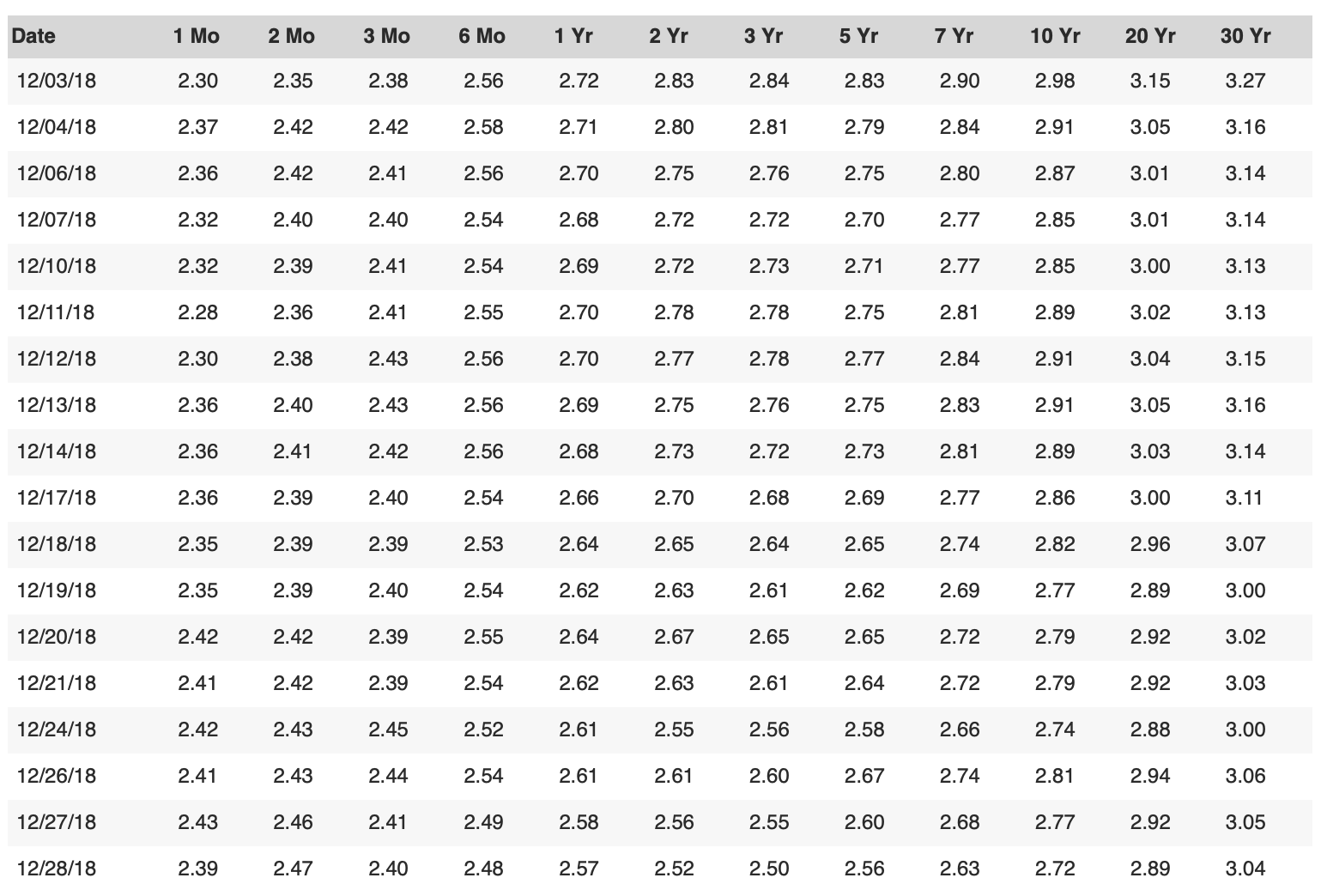

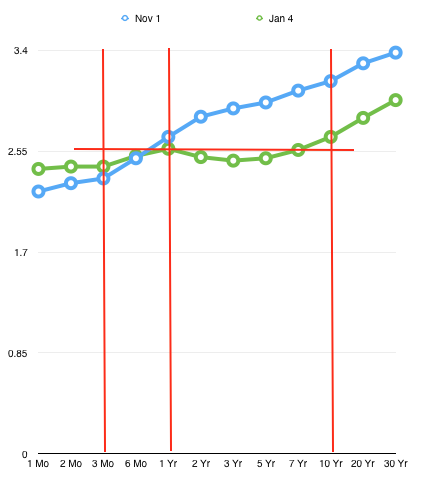

Since 1955, yield curve inversion is a forerunner of recession

Every recession of the past 60 years has been preceded by an inverted yield curve, according to research from the San Francisco Fed. Curve inversions have correctly signaled all nine recessions since 1955 and had only one false positive, in the mid-1960s, when an inversion was followed by an economic slowdown but not an official recession

This is information sharing purpose, do not take any action (Buy/Sell) based on this blog message.

I believe this is part of why “the smart money is on bonds” is a saying. It’s the buying/selling by bond investors that inverts the yield curve. They know and move in advance of the recession.

In 5 months, you will be out. Is it in time to avoid the crash?

In 5 months, you will be out. Is it in time to avoid the crash?