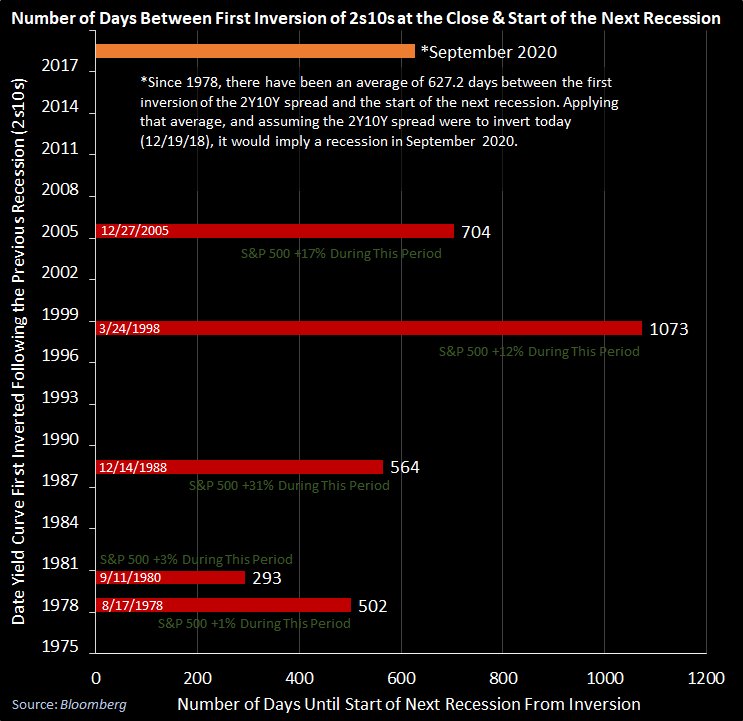

Why do FED wants to push economy into recession? To prevent depression?

Just in time to torpedo Trump.

This is my guess work or analysis, no data back up.

It is not FED putting economy into recession. Companies (75% of S&P 500) are producing better return than last year, i.e., economy is doing great. FED is increasing the rate based on economy data, unemployment data.

FED will hike two more rates, may be in Mar and Jun, leave it there to further to market to fall or recover.

But, Mr.Market (Market makers Hedge funds, Mutual funds, banks/institutions) selling investments and moving into cash position fearing possible future recessions by uncertainties such as Rate hike impact (how much), trade-war impact, br-exit, china economy and emerging market economy issues.

Remember, AAPL is increasing revenue from 63B to 88B-92B, but Mr.Market is dropping down from $232 to $160. This is done by Mr.Market, not by FED rate hike.

Mr.Market is pre-empting that brings down the market. This pre-emptive action is good as we may not have year 2008 effect of deep recession.

Remember FED Powell was telling we will hold below normal rate for longer time. This means market has to come up on their own, no rate reduction unless it goes too much negative.

FED will hold the rate steady for longer 5 more years. Why rate hike? If they do not do, we will end up like Japan. They wanted to avoid it.

Feel like hedge funds play it safe, locked in profit and their bonuses. So no Santa Claus rally. Let see we have Jan effect i.e. market up in early Jan.

Not only hedge funds, but by all institutions, banks, mutual funds…etc.

With this 13% S&P crash, I am not even seeing any activities in reddit and other forums including our forum. Lot of people are speechless, seeing loss after loss.

Bitcoin came down and will be crashing.

Cannabis was dropping and will be going down further. See TLRY, with 10M revenue, company went up $295 (12B Mcap). STZ going down with CGC investment…etc. MO is going down with CRON investments.

I have seen one person making 100k into 700k, but lost entire 700k in another bet ! Such Wild calls, spreads in reddit is completely gone as they almost lost entire stake.

Now, no one will come forward to buy FEDEX at dip, nor FB at dip. Some time market may come up, but other will sell it. We will see free fall easily.

Market will see the reality only when they see better than expected results in quarterly results. It is again depend on what the company results are and future forecast.

To talk more negative,

Now, shutdown voting is clean and fine, that is good. If they shift to Feb 2019, then it will mix will market results.

At that time Trump should keep quiet with China issue as Mar is deadline for 90 days.

1031 = deferring the payment of taxes owed during a real estate transaction.

Of course you can “remove” your money even if you are not 59-1/2 from any deferred account or program.

Most people, based on their ignorance, are afraid to cash in their 401Ks thinking the older they are, the better, they won’t be paying taxes. You can’t avoid taxation. ![]()

One thing is getting taxed as you should be in a deferred account, another thing is paying 10% penalty for not being of an age to withdraw it.

The 10% penalty can be avoided by a rollover. From the “instrument” where you rolled over your $, you can withdraw it slowly so you are not increasing your tax bracket. Basically this is done with people close to the 59-1/2 age.

When you retire, good luck with your income, it will be taxed if you earn more than the guidelines. This is something people on this forum are trying to ignore, or talk about it, but it will eventually bite their buttocks.

Nothing beats life insurance. You paid taxes already, so the income is not taxable.

This is an old copy I have that explains the details, tax bracket may be different but the concept still applies.

Both statements are wrong.

First, Forum people are not trying to avoid, they know the truth.

But, they do not like to counter as you may not understand the benefit or IRA/Roth/401k

Second, your statement “You paid taxes already, so the income is not taxable”.

This is exactly like Roth IRA/Roth 401k which will easily defeat Life Insurance.

When they retire after 59.5, they can easily take the money (as there is no tax) or grow non-taxable way.

It is their own money and they do not need beg the mercy of Insurance.

Roth growth, it is up to their skill set

It is the best way to grow our money tax-free for retirement.

1 Like

This is exactly happening like the Obama Period, stalemate at US congress+White House.

WASHINGTON—The Senate on Wednesday night passed a short-term spending bill that will keep the government open until early February, setting the stage for a fresh fight over border-wall funding in next year’s divided Congress.

The stopgap bill passed the Senate on a voice vote, with lawmakers from both parties eager to avert a partial shutdown when seven spending bills expire at 12:01 a.m. Saturday. The bill extends funding of the government until Feb. 8.

The measure now heads to the House, where it is expected to be passed on Thursday. If signed into law, the measure would extend a monthslong fight over President Trump’s campaign pledge to build a wall along the U.S.-Mexico border into next year, when Democrats take control of the House.

Jil, I know you are a smart man, always trying to help your comrades on this forum. I admire you for the knowledge you have on RE and the stock market. I am not kidding you, I have great respect for the information you give them, but on this issue, and the political arena you are naïve and a little bit out of current and factual information, we all are at some point of our lives. Mea culpa.

Now, I understand your reasoning on calling life insurance a fraud, and calling me a fraudster. You need to research better. You may cause people to lose their well saved/invested money. A good advise to you, leave that to people who know their game, or are sure about what they know, even 60% will help.

Out of life insurance, nobody, no retirement program will avoid paying taxes. The difference is that the ones you promote are retirement programs and the one I promote is life insurance than can be used as a retirement program under the protection of tax code 7702.

Your own money, 100% is at the hands of the provider of your programs. You can loan $, but be in danger of being taxed and penalized if you don’t pay the loan on time. And you lose the profit on that loaned money.

With me, only 20%-25%. The rest you get it in your hands, and the same amount is still there earning compounding interests. You pay a premium of $100, you get a leverage of $160. 80% in your policy earning 4%-12%+, and 80% in your hands, and because you are good at the stock market, you can make a killing with free money. Didn’t you see returns of 32% posted by some comrades on this forum?

You are bundling Roth IRA/Roth 401 and even 401K as if people just grab their money and run away without paying taxes. You are trying to fight the real fact that only a well planned life insurance shields you from paying taxes ever. The other programs tax you on the returns or profits, worse than that, when you are retired. Read about tax code 7702.

Then, your principal is at risk.

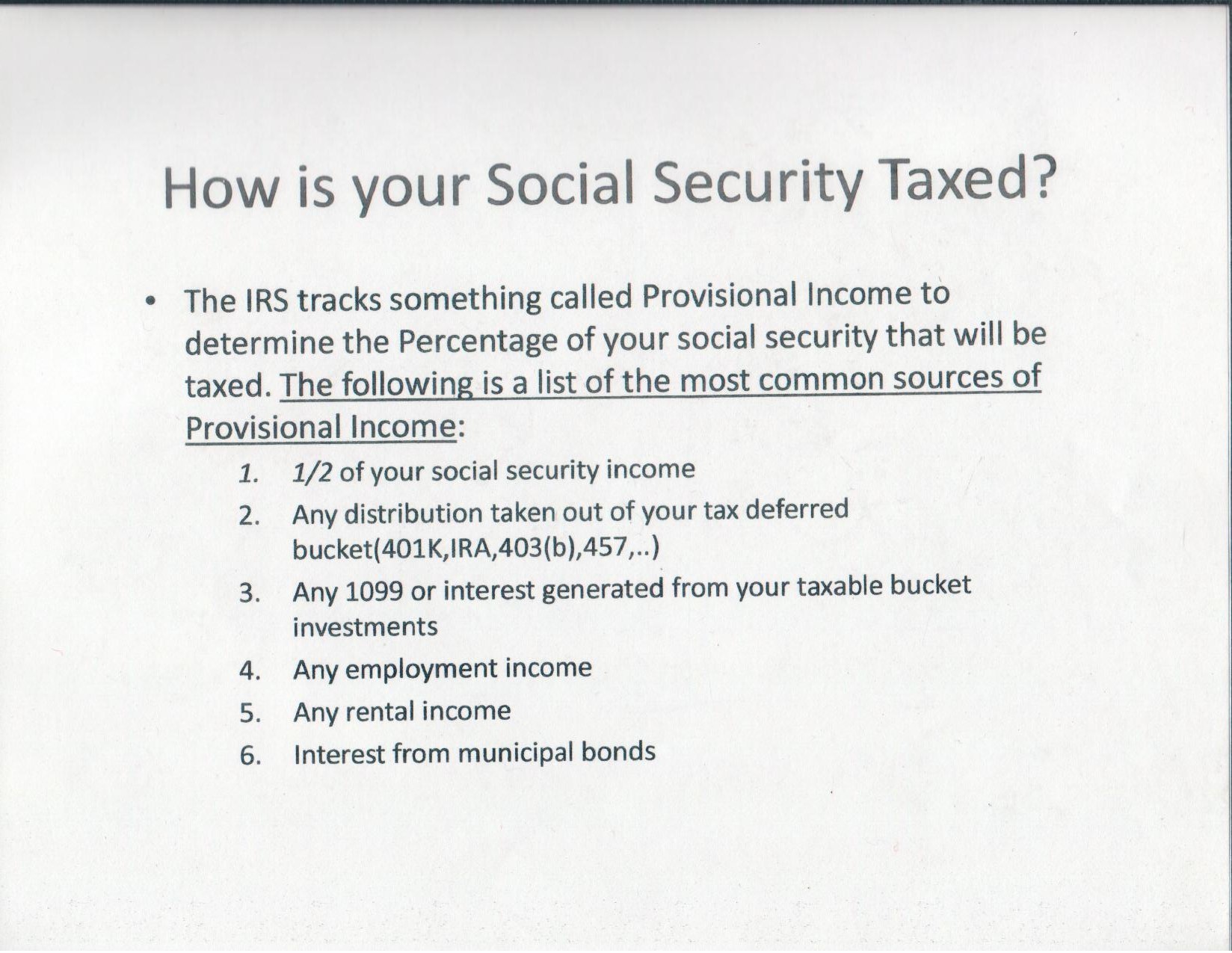

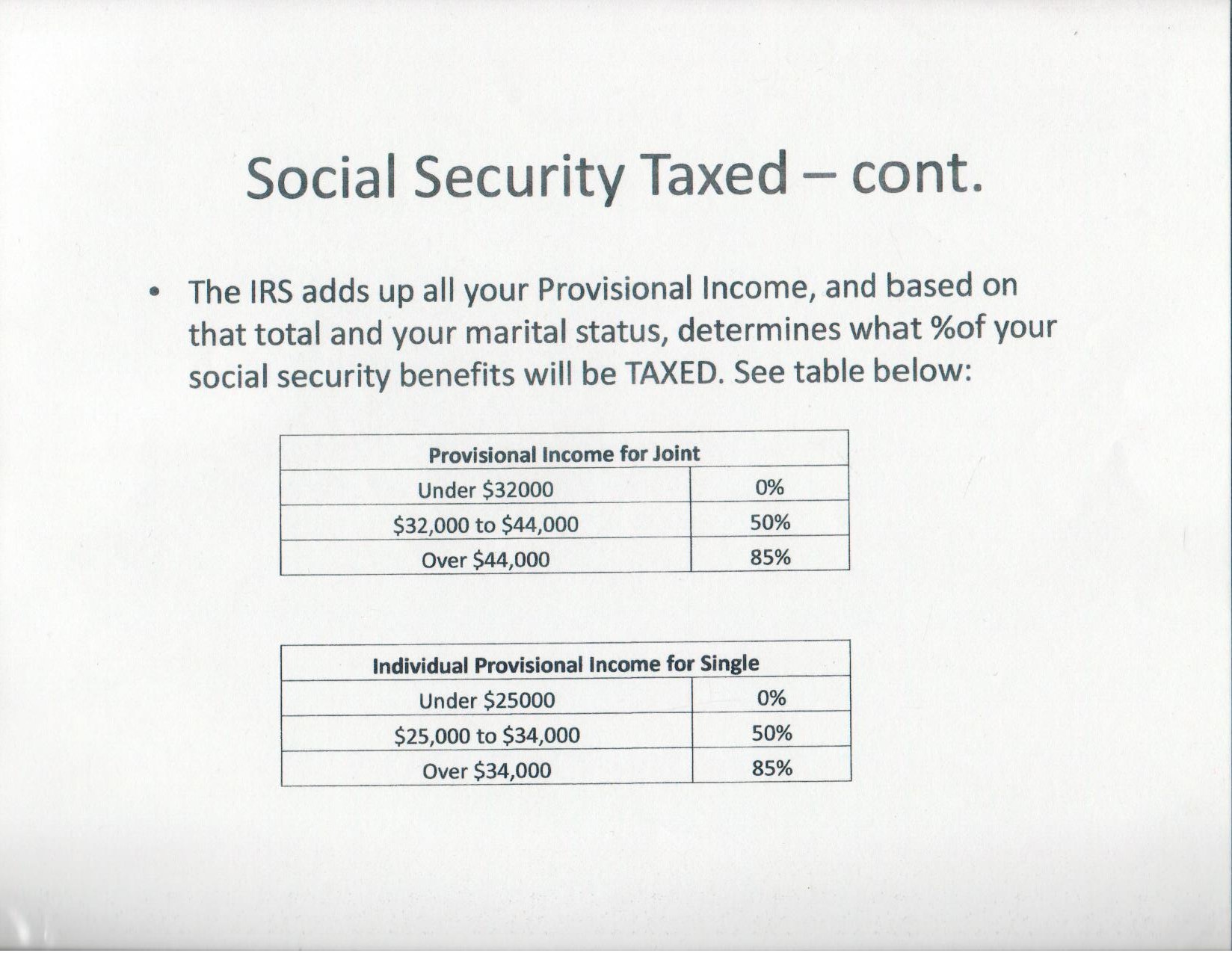

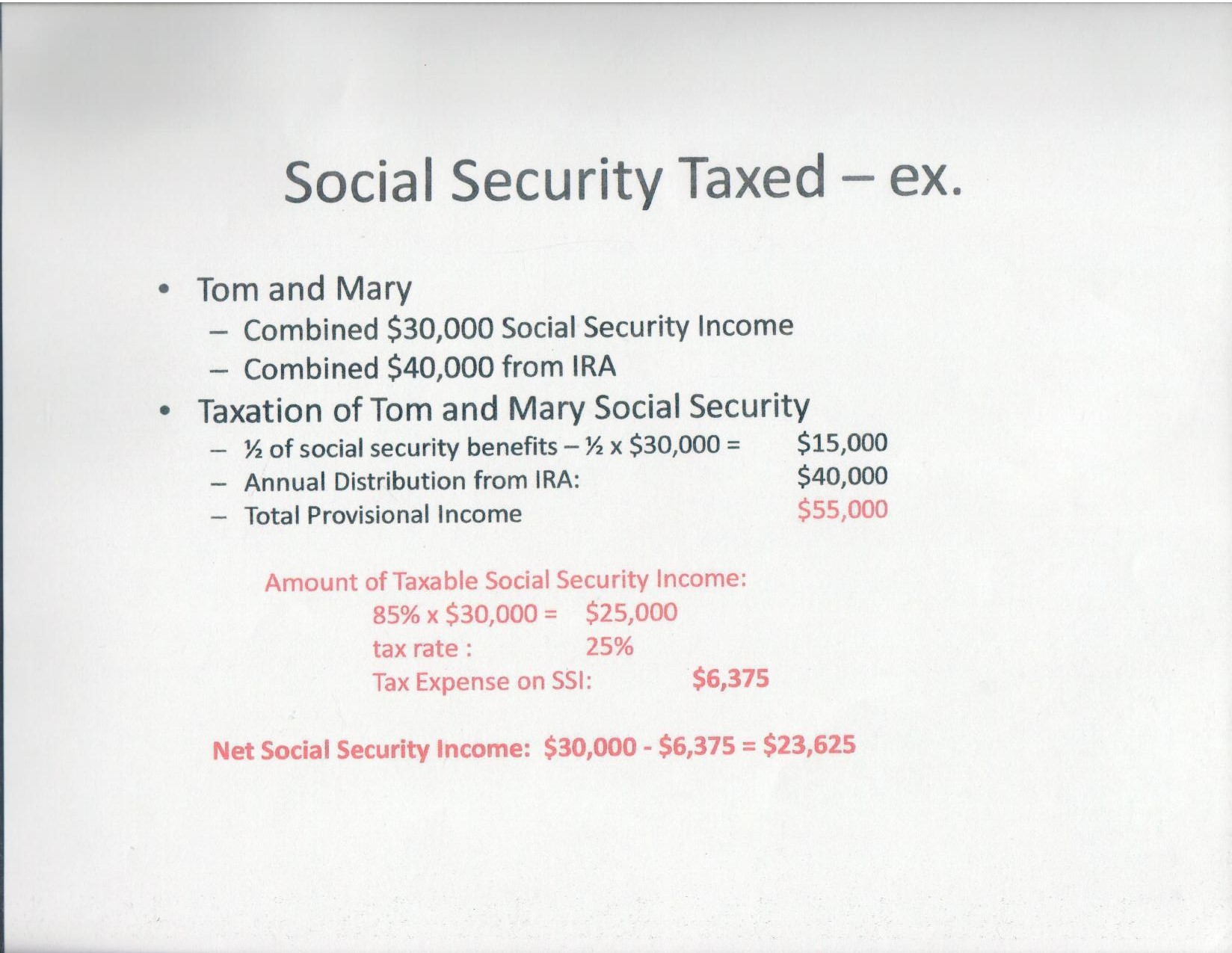

Higher fees are forever. It doesn’t matter if you are retired, the fees will be eating your 401K since you are not contributing anymore. Yes! you are stuck to minimum distributions and get penalized with due taxes if you withdraw everything. Your tax bracket will increase taxing your SS check up to 85% as described above.

On the other side, in an IUL, there’s no limits on the contributions, they are based/according to your income and work history, health, age, etc. You can contribute lots of $ and you get a hold/loan of 75%-80% of your own money right away, in days, never to be paid back ever!

In an IUL. Zero is your hero, you don’t gain/profit when the market crashes, but you don’t lose your principal either. Period! (I know, there’s a premium to be paid, interest on the loans, that is established, but the interests are paid by the death benefit using the loans as a collateral).

Can your other programs avoid the market crash? Answer me please.

Wrong #1

“”“You can make or lose money in any kind of economy, and it doesn’t matter what type of investment account you use. A Roth Individual Retirement Account (IRA) is a useful account type because it shelters your profits from taxes until you withdraw them from the account. How you fare in a bad economy or recession depends on how you invest. In fact, certain investments, like bonds, can make money when the economy drops.”" <-----positive fact from it, that’s all ![]()

Wrong #2

Roth IRAs

Unlike a traditional IRA, a Roth IRA doesn’t give you a tax deduction on the money you contribute. It does postpone taxation on your profits until you withdraw them from your account. You pay taxes only on the profits, whereas you pay taxes on all withdrawals from a traditional IRA. Also, a traditional IRA makes you start withdrawing money at age 70 ½, but Roth IRAs have no such requirement. Income limits apply to Roth IRA contributions: If you earn more than the limit, your contributions are curtailed or disallowed.

““You pay taxes only on the profits””

See Jil? You pay taxes at the end on your profits, plus fees month after month? IULs? 7 years down the road the fees are decreasing to be non existent by the income.

More to come. ![]()

The troll always forgets the interest the IUL charges you to borrow your own money. The troll also ignores that you can in fact lose money if the IUL investment gains are less than the interest charged to borrow the money. That happens in ~40% of years. Some how the troll thinks paying all that interest is better than paying taxes. The troll loves to mention the invested money grows with compound interest, but ignores the loan also grows with compound interest. That makes it far worse than taxes.

What’s wrong with this forum? I speak to Jose, and Maria responds?

The Russian troll doesn’t refute what financial experts know about those deferred programs being pounded by the stock market crashes. The ignorant troll doesn’t understand that the interests on the loans are paid for by the death benefit that is increasing year after year to accommodate the loans. Easy money to make.

And, the Russian troll doesn’t know that you don’t need to make a loan, and if you wish too, you can only pay the premium, and even not pay premiums at all since the returns are enormous.

What can you expect from a Russian troll trying to beat an illustration approved by the department of insurance, the poor bad spread sheet maker trying to bet a mathematical algorithm sanctioned by the government?

702(j) Benefits – Tax Advantages in Retirement

Life insurance has amazing tax benefits for you in retirement, including the fact that it does not have a required minimum distribution amount, which makes it superior to 401ks and IRAs in this regard.

- 401k plans and IRA plans require (i.e. you have no choice) you to take out required minimum distributions (RMDs), which are taxed as ordinary income, i.e. based on your income tax bracket. The result is that your social security benefits may be taxed and Medicare part B premium penalties may apply.

https://www.insuranceandestates.com/7702-plan-770-702j-accounts-explained/

Wow!

The stock market is crashing big time! 570 points so far!

My clients are protected.

I posted the math on how much more money someone would have by buying 20-year term life insurance and investing the rest of the money in SPY. It was millions more than your way of doing things.

I’ll never be able to explain these financial things to you, but everyone else realizes what you’re portraying isn’t accurate. That’s good enough for me.

2 Likes

If you ever attempt to show me another of your dumb spread sheets, I swear, I will turned into Muslim.

This forum is not only for you dummy. You are portraying yourself as if everybody agrees with you. Let them speak their minds with counter productive arguments, not “I don’t like it, so it’s enough for me”.

Dumb, dumb, dumb!

How old is Jil?

He should be by now read my counter argument and he should be ready to counter my argument too. Unless he is lost in the limbo of that wrong concept of no tax that is going to hurt him when he retires because he thinks he just will close his accounts and no taxes to be paid. Really?

When you do not have counter arguments, you will ask nationality or age or some nonsense!

Do not think you are smart, next two years will teach you big lessons! If you survive economic headwinds next 2 years, we can discuss after 2 years.

2 Likes

I think I would tell you that Marcus is old enough to respond to whatever, so, mind your business and stop spinning. Respond to the screw up you created by telling other innocent people they wouldn’t pay taxes when cashing out their deferred accounts.

That is wrong, absolutely wrong!

You are hurting people with your unfounded advise.

And, learn to be humble and say thank you when somebody praises you.

I totally understand what you are trying to do. You do not have data points to counter, that is why bashing me and Marcus !

We both counter you whenever you try to display IUL is great against 401k.

Whether we counter you or not, forum members have sufficient intelligence to know what is good for them.

2 Likes

OK Jil, you keep hammering a losing argument.

Again, learn to be humble and say thank you. That is what respectable and people with decorum and dignity say when they are complemented. And, the Muslim thing was a joke, what’s the matter with you? I know Marcus is a racist so I tried to get him riled up because he hates them, he is a republican! And he hates minorities too.

And, you were wrong!

You are so ignorant of the core aspects of deferred programs. The word “deferred” should give you an idea that taxes need to be paid “later”. Jesus!

For instance. Nobody is retiring “after” age 59.5. You need to specify “when”, it is to broad of a statement. Is it 60? 61? 70? 72?

That people can “withdraw” their money around the age of 59.5 is true, with the subsequent taxes to be paid. They are avoiding the 10% penalty but taxes are due, oh boy! The withdraw will increase your tax bracket, big time! And that increase will create a taxation on your SS check.

They will be paying taxes no matter what. There’s no law, rule, tax code that can help you to avoid being taxed on either the principal or the profits/returns.

Stop telling people they won’t get taxed with those programs! They will! Only life insurance avoids taxation, and probation! ![]()

You do not deserve that !

You do not read or understand my statements. Here again I provide you

Your statement “ You paid taxes already, so the income is not taxable ”.

This is exactly like Roth IRA/Roth 401k which will easily defeat Life Insurance.

When they retire after 59.5, they can easily take the money (as there is no tax) or grow non-taxable way.

You do not have any clue about Roth (neither IRA, neither Roth 401k). With your half-baked knowledge, you try to say retirement savings are worthless.

You are completely wrong (and do not understand anything about retirement savings) on Roth Side too.

Since regular retirement avenues are far better than IUL, the retirement assets are running into Trillions (almost 28 T) while IUL running in Billions !

3 Likes