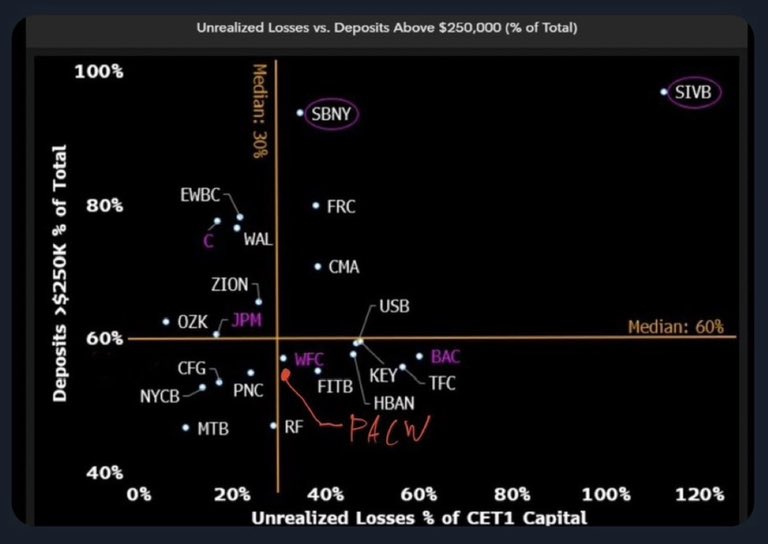

Is BAC’s unrealized loss really at 60% of their Tier 1 capital? Didn’t fact check. Sounds kinda dangerous.

I’d really be surprised if BAC was experiencing that kind of loss. I was with BAC from 2014 to 2020. Once pandemic rate pressure hit and everyone started funding 1.x rate 15 year loans and 2.x rate 30 year loans, BAC was keeping rates in the 4’s. They did not want to join that party and for good reason In early 2021 BAC reduced their rates into the 3’s and finally got back into the market. It was a short window of opportunity for them as 2021 was the beginning of what is now our present rate environment. BAC perhaps bought servicing, but that would be unusual. They weren’t in the 3rd party origination game either as WFB was at the time. I could see that kind of loss for WFB, but BAC? Need to see more info than just that chart.

3 Likes

But is the loss really from mortgage originations? My understanding is that most of the loans are packaged and sold rather than held on the books, including jumbo originations. In the case of SVB it was underwater 10-yr treasuries that got them, which is ironic in the sense that treasuries are supposed to be the safest paper you can get. Would imagine that most of the other bank losses are also due to medium and long term government bonds rather than mortgage originations.

1 Like

I found this Barron’s article from last week talking about BAC’s unrealized losses:

Archive link:

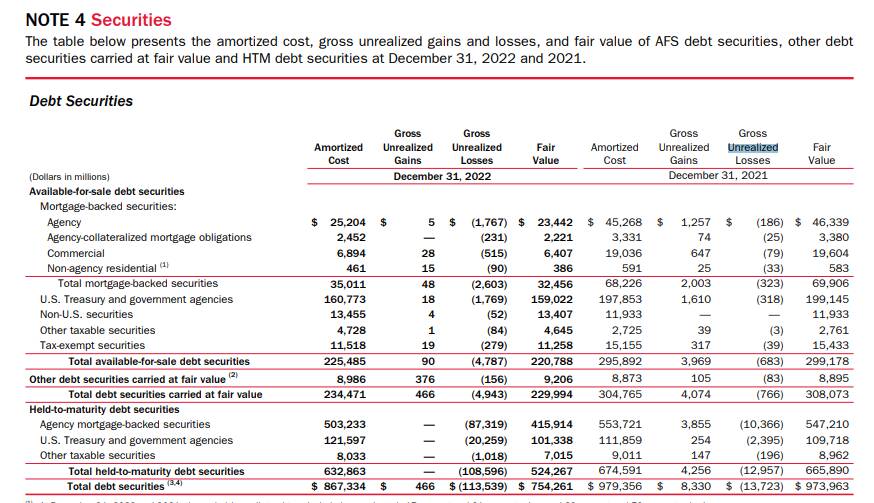

Bank of America had $862 billion of debt securities on its balance sheet totaling roughly $3 trillion at the end of 2022. Of that, $632 billion of bonds, mostly federal agency mortgage securities, were classified as held to maturity for accounting purposes.

Banks don’t have to record losses on changes in those securities’ value, cutting into their capital, unless the debt is sold. Still, holdings in that bucket, which carry minimal or no credit risk, were nonetheless showing a loss of about $109 billion at the end of 2022 due to the rise in interest rates over the past year.

This compares with losses of $36 billion for a similarly classified bond portfolio at JPMorgan Chase (JPM), $41 billion for Wells Fargo (WFC), and $25 billion at Citigroup ( C) and just $1 billion at Goldman Sachs Group (GS), based on each company’s 10-K filings with the Securities and Exchange Commission.

It’s fundamentally a liquidity issue. Banks don’t need to sell these supposedly “held to maturity” securities if they have enough liquid assets to honor depositor withdrawals. Things got ugly when confidence collapsed and people withdrew 42B in one day. That’s why we need FDIC to increase deposit insurance.

2 Likes

And by the way, as the Fed keeps going down its rate hiking warpath, those underwater bonds will get even more underwater. So the pressure on financials will get more acute with every hike.

If an underwater bond is held to maturity the loss is the same as if it was sold. The difference is whether the loss is realized as a capital loss or absorbed as a real loss (opportunity cost, inflation, etc.)

All other things being equal one is better off selling underwater bonds likely to stay that way before they mature. Capital losses can be written off; real losses can’t.

Of course the paradigm under which banks operate is totally different from that of investors.

Depends on the time of sale and rate on the market.

If I have 10 year bond at 5% Apr, meanwhile FED rates are increased 2% holding for 2 years and then reverts back to original, then my bond value goes down during that period alone.

If I am forced sell, to meet depositor demand, I am a loser. If I hold until maturity, I still make money.

This is exactly like long term buy and hold of stocks.

For example: I bought 6 months $500 T-Bull , but they charged only $487.50 as this is the price of auction.

At maturity I will get $500 after six months whether another 6 months T-Bill sells at either $450 or $550 does not matter.

Things look a bit different over longer periods. Someone who bought the 30 year in the late 40’s and held to maturity in the late 70’s suffered a huge loss in real terms.

I do not deny this, but banks are operating under net interest margin.

They pay very low rate on deposits, appx 1.5% less than what they are getting from long term bonds. With .25% FFR, they gave 0% interest on deposit and getting 1.5% for 10 years. For banks it is always plus when they hold until maturity.

It is not because bonds banks failed , but by frenzied withdrawals on a single day !

2 Likes

.

![]()

So banks need to be disrupted and restructured ![]() More accurately, services provided by banks need to be done differently.

More accurately, services provided by banks need to be done differently.

Now, after system is broken, banks will dictate limits on transfer and come up with rules to comply.

1 Like

.

There are already limits for ATM, EFT and Bank Wire.

For certain privileged accounts, bank wire can be unlimited ![]() Guess, now have to put limit on them.

Guess, now have to put limit on them.

PACW down 17% today.

PACW is on this Michael Burry chart:

T-Bills, T-Bonds, MBS are normal way of investments. With year 2008-2009, all risky wild options (CBO kinds) are ruled out by banks and they are not holding anymore.

Schwab is well known broker next to Fidelity and Vanguard in terms of transactions, USB is also owned by Warren Buffet.

I like NYCB, PACW and FRC (high risk) and ETFs XLF, KRE & DPST. These are available at recessionary bottom now.

IMO, this is the last leg opportunity, for at least next 3-6 months, to buy these bank stocks at low price.

I have PACW, DCAing PACW today and will be tomorrow too. All these bank stocks will not long last and they are about to go up by end of this month.

BTW: Apr 15th onwards Bank results start.

I am not sure this is the last leg. JPow is still hiking and Yellen is reluctant to go ahead with FDIC Infinity.

Wonder if any bank will collapse this weekend.

PACW’s chart looks like this. It already fell through Covid low and just a hair above GFC low.

Being country financial heads, they do not want to commit to public openly as market will go zooooom if they do !

When FED declared Mar 23, 2020 unlimited printing, how market went V-shaped recovery. They do not want to see such as it will work against inflation fight.

But, both of them trapped by SVB collapse and maintain a balance.

No, not at all. Market has hit the bottom of this cycle by Mar 13th. Today dip will end up bottom tomorrow end of the day. Since last 3 days market went bullish silently, there may be lot of short term (friday) calls and all will be worthless by tomorrow end of day. This sudden drop is well expected and I was waiting for it to happen (selling all stocks two days before).

PACW has the risk (small banks), but I like it (somehow I do not knwo why). At the same time, I too NYCB at 6.5 - 7 price range, I am DCAing now.

However, future is always challenging, but at some point we need to take some calculated risk. I am just allocation max 15% of overall portfolio for these buy & hold banks.

Important challenge is once we purchase it, never be scared by market and hold strong until recovery!

KRE and DPST must fly like TSLA as I see similar pattern!

But for KRE and DPST - completely for trading 50% allocation, rest TQQQ/QQQ/SMH.

What do you all think of SCHW? They apparently have 18B of losses on books but not sure if they would have liquidity crisis or not. They can be 2x or 0x easily ![]()

On any case, you need to do research on this issue before investing. Here are my 2 cents.

I bought SCHW when dipped and sold it for profit already. The company is too good like MS, GS, Fidelity and Vanguard and they have bigger client base after taking over TDAmeritrade. I still have accounts with SCHW, TD Ameritrade, but do not like to hold long as the dividend was less than Treasury returns.

However, I do not think they will be insolvant risk, neither going to bankrutp stage with HTMs.

Better to listen the yotube

Balance Sheet - Will The Company Survive?")

These are HTM, as long as they hold until maturity, they will have the money. FED has almost stopped rasing rate and when FED reverses after 2 years, these book losses will be reduced (likely but depends on that day rate).

Personally, I am not concerned about HTM as this is common to all bank (all over the world issue), but no one can guarantee when 20% deposit withdrawal is happening to any bank !

When I tried to study SCHW, I came to how BAC manages such HTM securities…The big banks are hedging HTM risk with options

BAC has unrealized gains 8.3B while unrealized Loss is 13.7B and over all it comes down to 5B net unrealized loss.

If Hedged properly, they escape out of mess !

1 Like

Fed’s balance sheet continues to expand. Two weeks in a row now. QT now 2/3 reversed.

1 Like