is what the market thinks about…

Tesla Inc. revamped the Model 3 sedan with sleeker looks and longer range while slashing prices of its premium vehicles in an all-out push to boost sales.

Avg sale price declining >> lower margin >> lower net income… to meet EM’s production delivery, wonder how long before TSLA can’t make money with this price war.

I said years ago they were a car company, and their margins would end up the same as any other car company. They had a fun run of hype though.

Amazon is a retail company and their margins would end up the same as any other retail company? ![]()

Have the retail margins improved? They used to be awful. The AWS margins are great. I think if comparing to retailers then the two have to be separated.

Tesla also has multiple verticals if you want to call them that other than cars. You might be right Tesla might be another car company, however based on my experiences making these simplistic comparisons to predict the future of any company is not useful(just like Amazon example was).

I haven’t checked, but retail margins might have gone up a bit in the since the pandemic, and if they have the margins will get down in a year or two as soon has the Biden free money is spent.

The new M3 looks like it’s grimacing at you.

Solar and batteries are not a meaningful percent of revenue. What else is there? Software and charging stations?

Right now. @Zeapelido would know more.

Is adding new features to the car, which in others you have to pay to get, like in my ICE car which is a “luxury” car after 2.5 years for even something as basic as maps, I have to pay. On tesla there are meaningful feature updates. “FSD” is nowhere near completion though.

A new revenue source with most US EV companies joining.

Car-Volume wise also, it seems other than the Koreans and maybe the Chinese(in the future) no one can compete IMO.

They have a lot of small but growing verticals. However the certainty we can apply to them in terms of future cash flows is uncertain. So the stock is going to stay volatile as long as massive uncertainty persists. To be honest, it’s got a pretty hefty valuations given its current earnings trajectory.

Tesla ASP’s have been absolutely taken to the backshed over the past year. Various reasons for that, but I do think when interest rates come down ASP pressure will go back up. However that probably won’t happen for another 6 months to a year.

Tesla Energy is a pretty clear, solid business. This has higher certainty of generating good cash flows, although the proclamations of 50% margins is going overboard. Sometime end of this year to middle next year, they will be delivering 10 GWh of Energy per quarter, margins are already at 18%. They are also beginning a second MegaPack factory in Shanghai that will likely start production by middle of next year. By end of 2024, they could be delivering at least 15 GWh of Energy products at ~ $350 / kWh and 25% gross margins. I think this is the base case, not conservative but not bullish either. This, annualized, would generate $3 per share.

While FSD as a robotaxi service is further away, I do believe FSD as an advanced L2 system that can boost margins will come next year. Let’s says half of the produced fleet next year (~ 1.25 million) pays $100 per month for FSD. That’s approximately $0.5 contribution to earnings for the year (assuming no increase in purchases from existing fleet, or anyone purchasing it outright). I give another $0.25 EPS for those.

So let’s say auto margins bottom out and flatline here (maybe a slight increase as interest rates go down). By end of 2024, on annualized rate 2.5 million vehicles produced, Tesla will generate:

$4 in automotive earnings annualized

$2 in earnings from Energy and FSD. I just used $2 even though I just forecasted $3.75

Means $6 in earnings being generated annualized by end fo 2024. With a forward PE ratio of say 50, that’s a $300 fair value share price. Not a huge buy signal from current. But if Energy / FSD produces as much as I originally estimated, you are getting over $7. Now you are getting over $350 to $400 fair value (in a year and a half from now).

There are many other avenues that may flesh out more money. Service margins, insurance, recurring revenue from Energy services, Tesla Powerwalls (not included in the Megapack estimate).

From a trading standpoint, there is a good chance some of those things play out and contribute a bit to increased earnings by end of next year. I am definitely not bullish this year, but you don’t know when investors will realized forecasted future growth to be up from current estimates. Forecast for next year is $4.72 - this will go up I think over time.

I currently swing trade to feel less volatiilty - I buy calls on big dips, and close and sell puts when I feel the stock has gotten ahead of itself again (which I just did yesterday). If the stock moons to $400 right away, of course I will lose out on a fair amount of that gain, but I won’t feel as bad as I did last year.

.

50 is too high. P/E always decline as company matures. I think 30-35 is more reasonable. At $7 eps, share price = $245. So market is paying next 1-2 year price today.

Interest rate would stay high longer. Won’t be 6 months to a year. More like 1-2 years.

A reasonable argument, but (1) it will come down to earnings growth rate, which if it is above 50% next year, will easily justify a PE of 50.

(2) If we think about not fair value, but what price the stock could get to in the hype cycle, I could easily see over $400 temporarily. The PE ratioe even went above 80 a month for a brief period.

This is why I will swing trade.

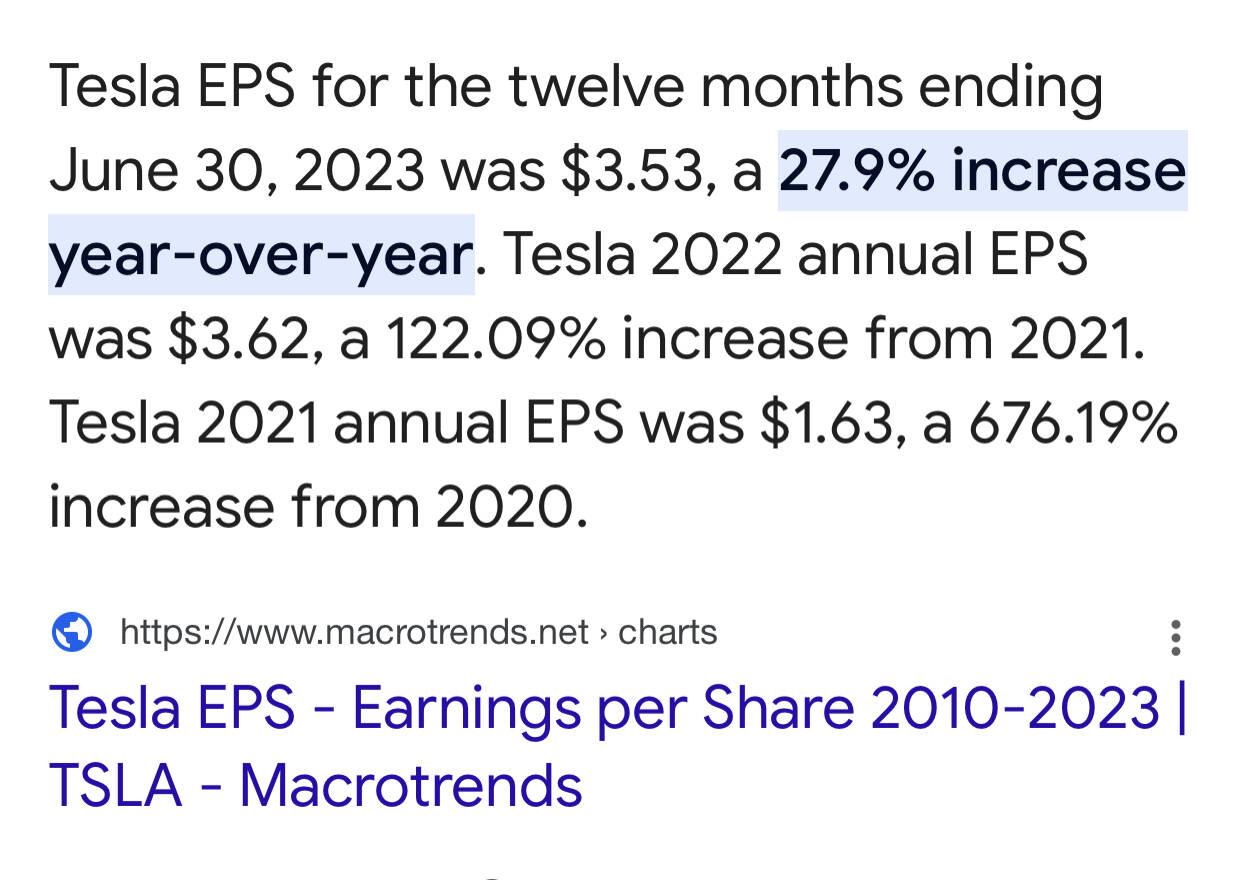

Tesla EPS growth is slowing down sharply though. May continue to decelerate.

Especially if Tesla continues to run its factories below capacity. Those depreciation charges could really hurt earnings, in addition to lower and lower margins on its cars.

Using options to buy insurance against stock decline is never a good idea. If you have conviction, buy and hold through thick and thin. That’s the only winning way.

Also, this is no reason to do it just because you “feel bad”. That’s letting your emotions get the best of you.

It’s so bad it’s funny. FSD tried to kill this dude not once but twice during the trip.

Even primitive systems like the one on my Subaru screw up. I’ve had mine lock the tires briefly because it couldn’t tell that the guy in front of me was turning off of the road and out of my direction of travel. Good thing no one was tailgating me. The next time I bust a windshield - which happens every three years or so on the Mogollon Rim for a variety of reasons - I may just tell the mom and pop shop to disconnect the whole thing and not reconnect it. Apart from collision avoidance the rest of the features are equally annoying and/or dangerous. Steering assist is a joke, cutting out the only time you need it (taking your hands off the wheel to fish for your coffee thermos). Lane keep assist is just annoying. Adaptive cruise slows you down way too abruptly when someone cuts in front of you and then takes forever to speed back up, annoying any drivers behind you. Collision avoidance was again confused on a dirt road last night, blurting out a collision warning when there was no danger of collision. Good thing it didn’t slam on the brakes again as it was raining and the road was narrow and muddy.

No, no insurance. I buy ITM calls with expiration about 18 months in the future. when the stock corrects downward signficantly, about 2x leverage. Then I close those out as the stock corrects back upwards, and move to 1x leverage and then less than 1x leverage by selling puts.

So basically I’m constantly long, I just vary the leverage coefficient based on stock price, momentum, sentiment, and my valuation over different time frames.