Above assume you stay and live for 30 ![]() years in the same

years in the same ![]() house.

house.

Frankly, at this point in time, not even sure is true for BA given very high price and low rent.

1 Like

Even if you only gain 2% inflation, you’re leveraged. At 20% down, a 2% gain in home value is a 10% gain on your principal. The biggest mistake most renters make is they don’t save the difference between renting and owning. Based on all the data, only a small percent of the population has that type of discipline. That’s why people should buy.

1 Like

If you assume appreciation is 0, let’s say you change house after 10 years. Appreciation is 0 so the two houses are of the same price. You can bring the principal you saved up in House A and use it to increase the down payment for House B. Instead of taking out a 30 year mortgage you do 20 years for House B.

In essense you are porting House A’s mortgage over to House B. The same marh will apply. Owning beats renting even with zero appreciation.

1 Like

Rent can increase but mortgage payment does not. So buy is better.

But the point is that when renting is cheaper than ownership cost, it means affordability is low so appreciation would eventually slow down and the peak is closer now than 2013

Are we still having the rent vs buy discussion? I thought the buy crowd won that argument on the old forum.

Renting is best if you can’t get the down payment and are uncertain about your future job prospects. Home ownership is the number one road to wealth. But if you have cheap rent in a rent controlled apartment then it may work out. Just buy a vacation home like in Tahoe to enjoy some appreciation…

3 Likes

Refer to the title: The question is “Does buy better than rent for primary works outside Bay Area?”

My 10-Year Odyssey Through America’s Housing Crisis

Misery over real estate hasn’t ended—2.5 million homes are still worth less than their mortgages. Here’s the story of one Wall Street Journal reporter’s upside-down American dream.

Still think “buy better than rent” works outside Bay Area?

0% may work, how about depreciation of prices?

Well, even for certain parts of BA “buy better than rent” for primary doesn’t work.

I think Shiller agrees with you. But the crisis was unique and I know plenty of people that got very rich buying in 2009-12. It comes down to location, timing and doing your homework. Buying a new house in a new subdivision in a marginally economically viable area like Mobile is never a great buy.

Buying in an area like Tahoe with an almost complete building ban, they only allow18 new houses a year. And 15m people less than 5hrs away was a no brainer. People that bought in 2012 have seen doubled house prices.

Didn’t make a statement or a position. I’m asking a question.

In other words, “buy better than rent” for Primary doesn’t work everywhere and all the time.

Like Shiller said no. But he like you are talking hypothetically. People live in the real world. On average homeownership is the best ticket to wealth in America .

I am a BA native. My grandfather got rich buying in Berkeley in the 30s. My dad was a horrible investor but he knew enough to buy your own home and hold on. He bought in 1961 in Berkeley for $53k. Could barely afford it. Now that house is worth $2m. Like my wealthiest friend says don’t wait to buy RE, bury and wait.

Most places in America are stagnant… places people are leaving. But some areas are growing. Takes local knowledge to know the market. That’s why I rarely invest out of state anymore

1 Like

I think most buy for stability not investment gains. That’s why most people don’t buy until they have kids and want to be in a specific school district. Who wants to deal with moving regularly with kids? Who wants the stress of having to quickly find a rental with specific schools?

1 Like

No, it certainly doesn’t in certain areas. I’ve seen it with my inner circle in places like parts of PA and NY. Should have rented but circumstances prevented that. Can’t sell to get back the money and so rented out for $1100. House only cost $160K.

1 Like

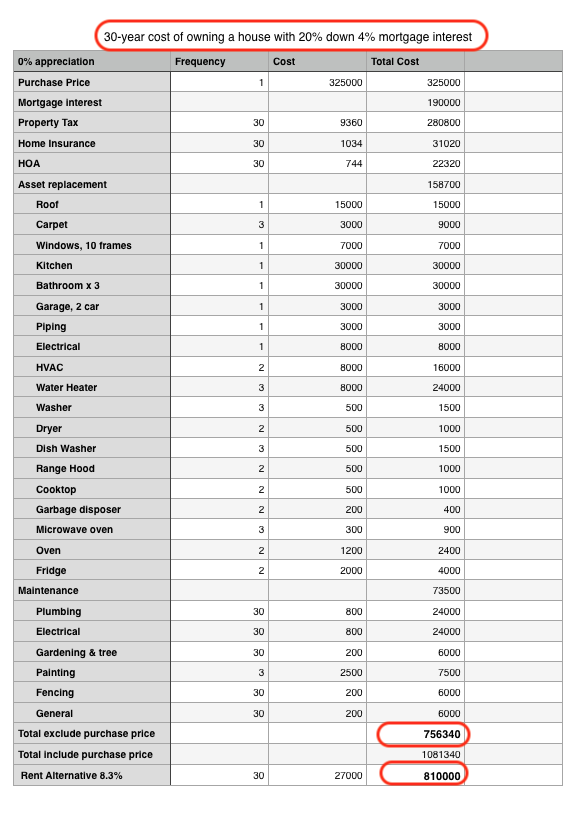

Refer to table below, for a family that has the necessary 20% downpayment and afford to borrow a 30 year mortgage with 4%, is it better for him to buy or rent (in Austin of course ![]() house price = $325k).

house price = $325k).

Assuming zero appreciation of house, hence also assume other costs like property tax, home insurance and HOA doesn’t change, and money if not put into downpayment & monthly PI is also earning zero interest/ return.

At the end of 30 years, renter pays more rent ($810k) than incurring all those costs ($756k). Both obviously would end up with the house, if you say is not, you’re not following the computation. Feel free to suggest changes to the costs (frequency, cost and missing items). I meant to prove both Harriet and manch wrong but guess they are intuitively correct. Anyone want to prove them wrong?

For non-zero appreciation of house and non-zero return of investment, we need to know which one is higher,

Appreciation of the $325k house vs Investment of downpayment + monthly PI. Obviously, the latter need to be at higher return than RE.

How does the renter end up with the house?

I’ve seen the analysis that says you’ll have a higher net worth if you rent and invest the monthly savings. I don’t disagree with the math. What I disagree with is expecting people to save the difference. 57% of people have less than $1,000 saved. Expecting those people to rent and invest the savings is a plan to fail. We already know they aren’t saving. That’s why most people will do better buying. The mortgage payment forces them to save money.

1 Like

Right. Any investment plan needs to consider people’s psychologies. Most people don’t save and invest nearly enough. Discipline is hard.

1 Like

Governs by the formula below. Can go either way.

1 Like

I feel like social media has made this worse. No one posts about the vacation they didn’t take, so they can save to invest. People post about things they spend money doing. Everyone thinks they should be living like that not realizing those people are a mess financially. Saving and investing is boring.

Any forced saving will do, such as an automatic plan to DCA into a S&P index fund.

In Singapore, we have CPF, is why there are so many millionaires in Singapore ![]() Many of us buy house using CPF too

Many of us buy house using CPF too ![]() Look at how high we save into CPF

Look at how high we save into CPF ![]()

1 Like

Automatic investing plan into S&P is not forceful enough. You can stop with just a button click on the computer. Many people stop at precisely the wrong time: near the bottom of the cycle. The psychological plan of seeing their account falling is too much to bear. It’s painful for me now and I have been at this for a while.

1 Like

You’re a control freak. I can’t even bother to look at it. Now that you said, I went in to check… $1.08M ![]() annualized return since 2002 10%

annualized return since 2002 10% ![]() about 2% higher than if have invested lumsum in 2002. Primary appreciates at 7% (only approxly, no data) p.a., so with a mortgage, Primary is better return

about 2% higher than if have invested lumsum in 2002. Primary appreciates at 7% (only approxly, no data) p.a., so with a mortgage, Primary is better return ![]()