If the worker who was WFH median 1 day a week pre pandemic now median WFHs 3-4 days a week , then these numbers have to translate to house prices too.

It’s basic common sense.

Speaking of common sense, Zillow’s massive fiasco on house pricing prediction shows data scientists need to be tested on understanding of their mental models of how the world works

3 Likes

I bet the model was fine. That’s why they weren’t winning bids. Then someone in management pressured them to “tweak” it, so they would win offers. They did and now we see the result. It’s the old management is going to make a decision, so come up with some numbers to back to scenario.

They likely trained their model on historical data and trends.

One potential problem could have been pandemic inducing new trends not seen in the data previously and then the model would suck.

I hear 2 views. One is of course model is not good enough which was developed by a Stanford guy. Another is model is very good but management didn’t take into account material & workforce shortage which lead to this mess.

Management definitely has a role + historical trend extrapolation and unprecedented situation(100 year event). Read that Glenn Kelman(of Redfin), laid off or furloughed many many people in Redfin @ the March2020 time frame, in spite of having so much data and expertise in the company .

Anyways, my main point was on house prices trend might match upto rental trends long term due to new WFH conditions due to covid even after covid goes away.

Data scientist point was in jest(indicated by the smile).

1 Like

3 bed, 2 bath, 1700 sq ft house on 6400 sq ft lot in Sunnyvale sold for $2.75M. Prices are holding strong and maybe increasing. Similar house may exceed $3M by spring 2022, given the high level of inflation

1 Like

They didn’t need that historical data. They were buying so may house they could have mined their own sales data. If you are winning every bid, you know you are paying to much. They obviously knew they were overpaying. They could have easily dialed back on their bids based just on the fact that they were getting too many deals. A very simple algorithm to generate. Seems like an upper management mistake. Heads should roll.

2 Likes

1 Like

Of course it will end when the market runs out of buyers.

Run out of buyers? Joking?

There will always be buyers, but not at every rising price. At some price point buyers will refuse to come in.

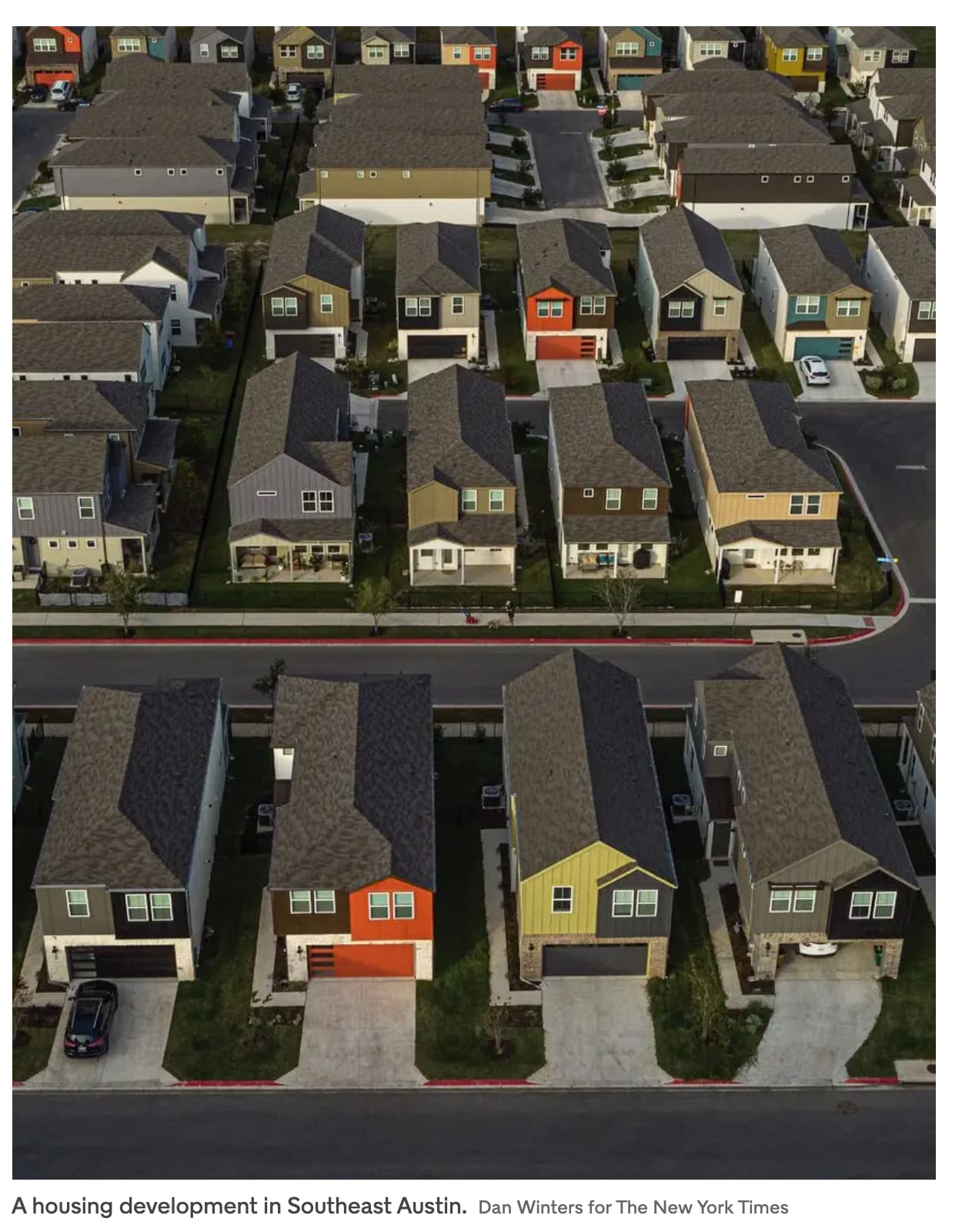

A great article. But this picture of Austin is kinda sad… so cookie cutter devoid of style.

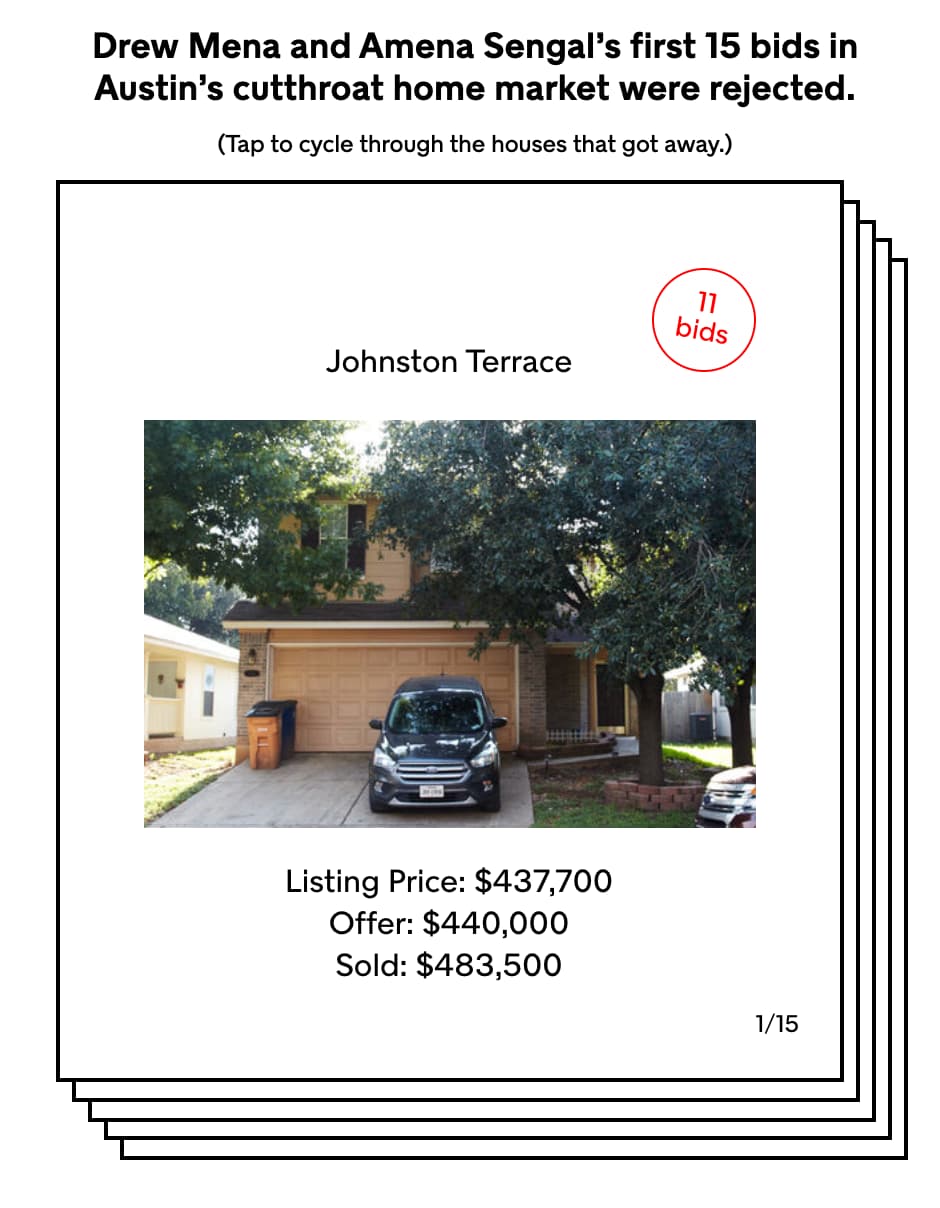

and this NYC couple tried to be cute and low-balled people, no wonder they didn’t get any.

Ppl keep saying TX has so much land. Why do they build homes like this?

They say Austin is the SF of Texas. But I don’t see neighborhood so ugly around here.

But a majority of investment buyers are smaller companies and individuals: mom-and-pop landlords, tech workers looking to diversify their portfolios, teachers who supplement their paltry paychecks by Airbnb-ing properties on the side. The ease with which they can access credit strains the market and drives up prices. Those effects are likely magnified when investors target homes in cities less expensive than the ones in which they live, whether they’re Chinese investors in California or Californian investors in Texas.

Greedy investors like @hanera?

![]()

Silicon Valley investor as the villain here.

![]()

The SV investor made the right choice. Invests in Austin but continues to live in the Bay Area.

Often, the person still standing was that most hated figure in the Austin real-estate market, the California investor. The winning bidder for Ephraim Road, for example, was Michael Galli, a Silicon Valley real estate agent. “Here’s the interesting truth,” he told me. “I’ve never been to Austin.” He toured the Ephraim Road house on FaceTime.

In 2019, Galli decided he wanted to diversify, so he spent eight months studying cities online and kept coming back to Austin. It had high-income job growth and an influx of venture capital, the very things that had made Bay Area real estate so lucrative. Galli bought a large map of Austin and mounted it on the wall, studying it in the evenings with a glass of red wine in hand. He stuck Post-its onto points of interest: Apple, Samsung, Tesla, new transit lines. He believed he understood what tech workers wanted: spacious feng shui- and Vastu-compliant homes, with a bedroom on the first floor to accommodate foreign parents on long visits. And most important, good school districts. He resolved to acquire 10 homes within a 12-minute drive of Apple. For $1 million down, he’d own $5 million in assets that he would rent out for top dollar and that he believed would double in value in five years and double again by 12 years.

3 Likes

.

1 Like