.

Another possibility is EM wants to start an AI & robotics company. Asking for the sky forces either he got 25+% controlling shares i.e. many shares for free or at very cheap price or he holds a large ownership of the AI & robotics startup.

.

Another possibility is EM wants to start an AI & robotics company. Asking for the sky forces either he got 25+% controlling shares i.e. many shares for free or at very cheap price or he holds a large ownership of the AI & robotics startup.

Good luck splitting those out separately, since TSLA already started the work. There’d be a shareholder lawsuit.

100% accurate description of the situation.

This article from Beth is pretty balanced and worth a read.

Beth reasoned Tesla’s auto margin is close to bottoming. Her reasoning is that Tesla’s margin should already be very close to GM’s in Q4.

Q3’s actual operating margin came in below that level, at 7.6%, landing between Honda’s 8.5% and VW’s 6.2%, while still sitting above GM’s 6.8% margin.

Q4’s operating margin is projected to be ~7.2%, for a ~40 bp sequential decline.

At that level, the spread between Tesla’s operating margin and GM’s would be less than 40 bp, adding evidence that operating margins are approaching a bottom. Aggressive price cuts look to be easing, a tailwind for ASP inflection, while declining lithium and Li-ion battery prices would add production cost reduction, a second tailwind for margins.

Knox’s TA analysis is pretty bearish for Tesla:

It’s worth noting the head and shoulders pattern that is close to confirming. This is the red count above, which implies that if Tesla breaks below $203, then the lower target will be sub-$100, as we likely press below the January 2023 lows.

Because to get people to switch to EV would require measures so coercive those governments would be voted out of office.

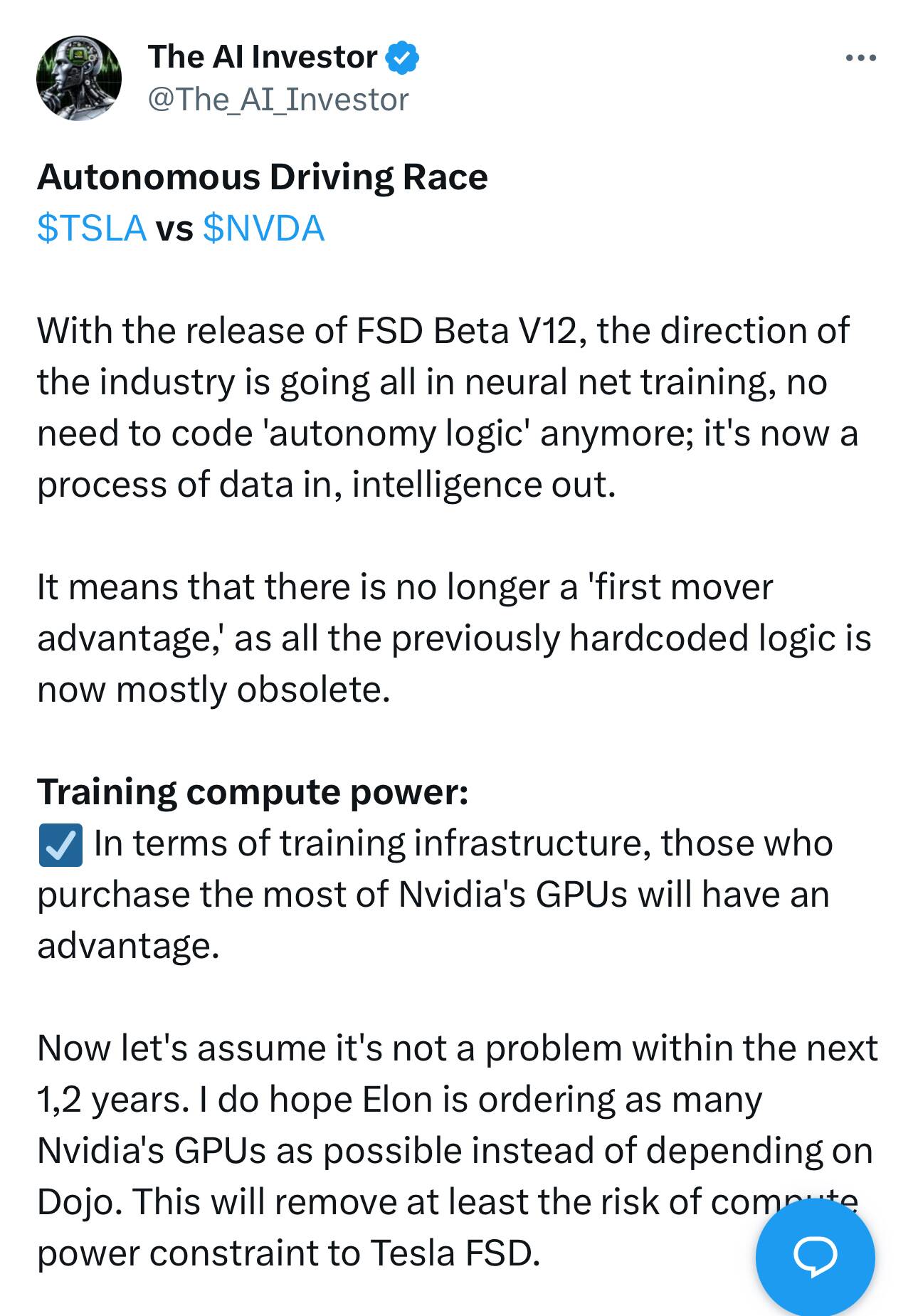

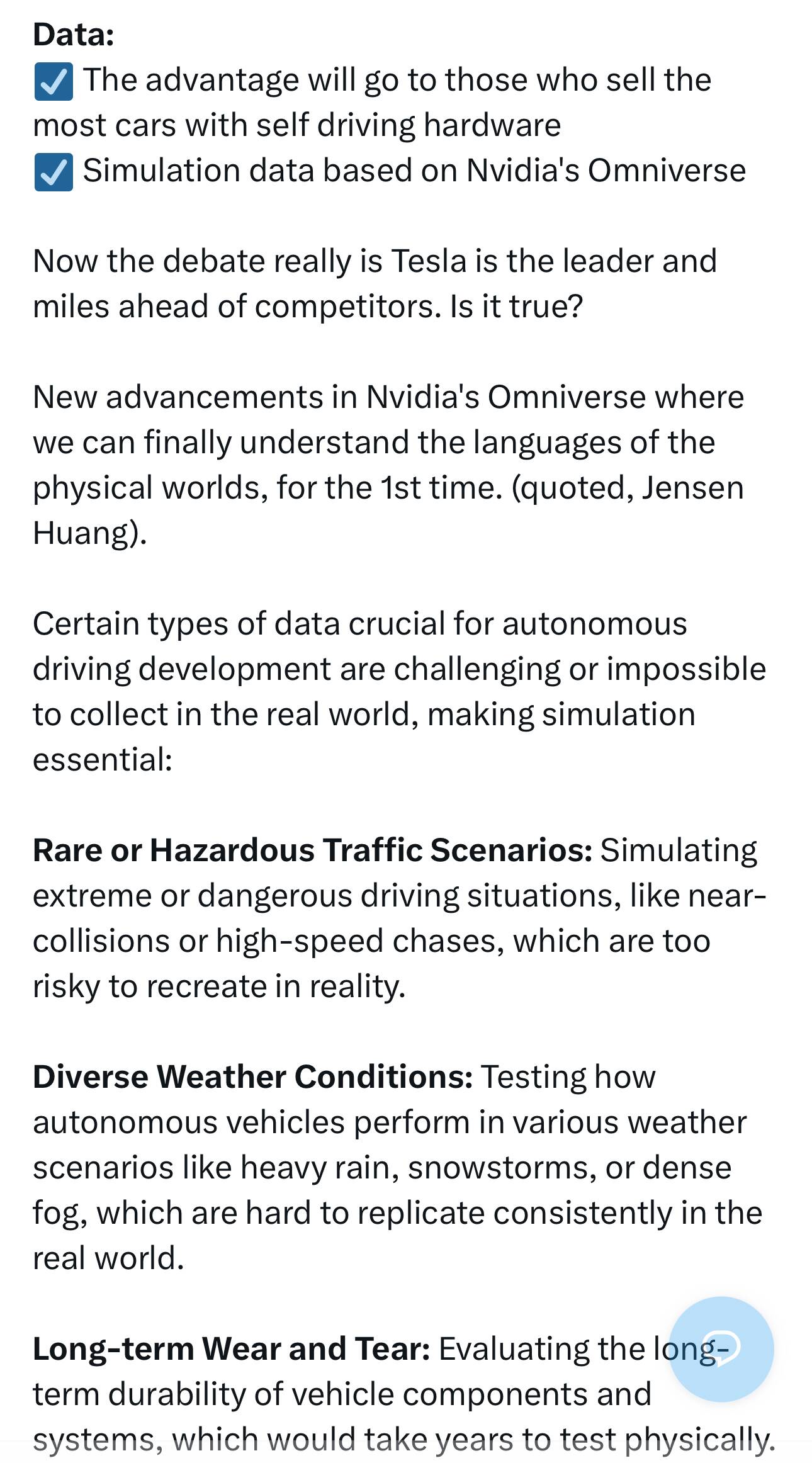

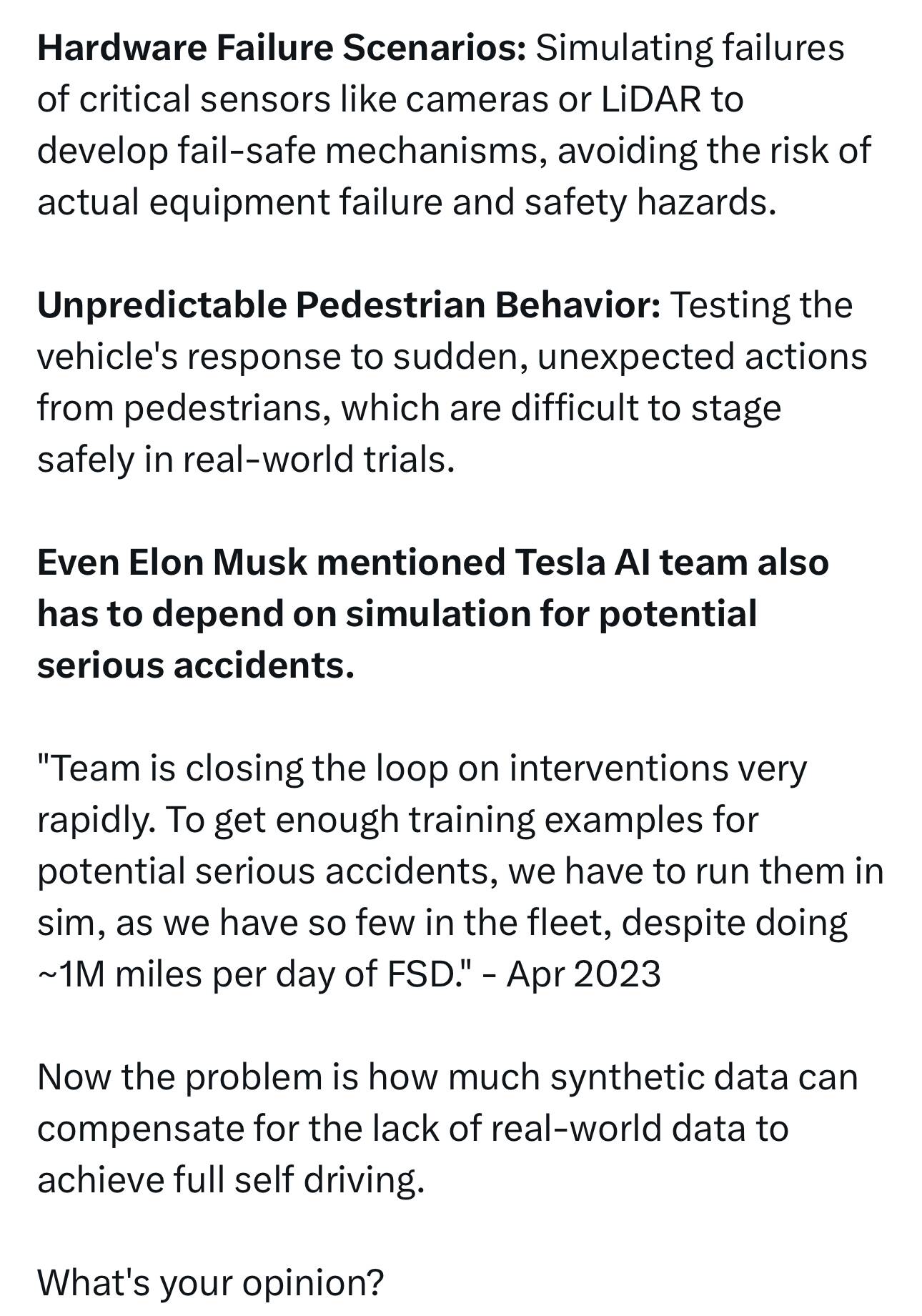

Um, they can’t get enough real data so they want to train FSD on simulated data. I can’t imagine what could go wrong.

FSD used routinely is at least 10 years away. Not a good investment strategy to value anything related to it. Personally I doubt it will be prevalent in my life time.

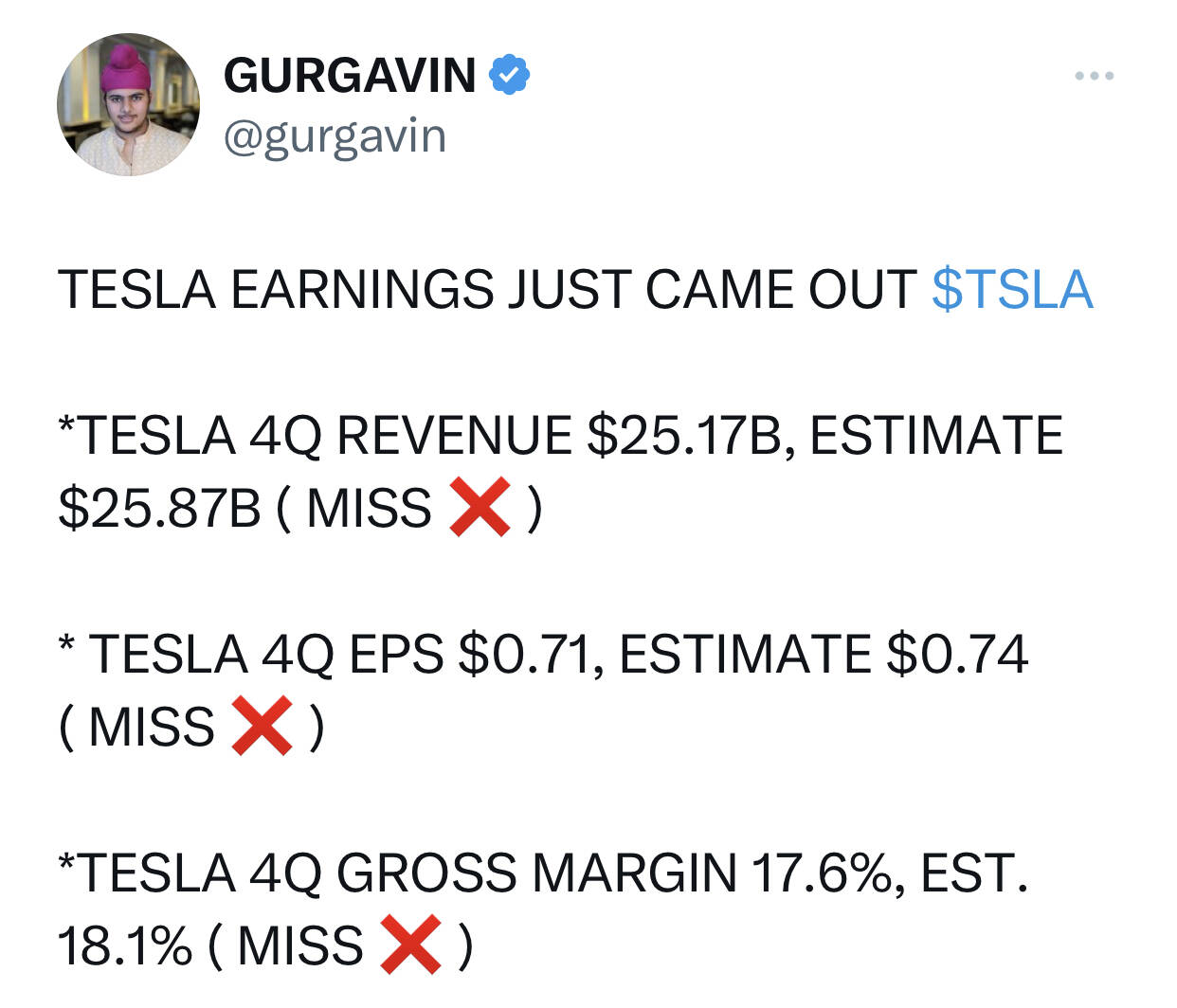

Tesla triple missed.

Volume growth will be “notably” lower this year. So low it refuses to give guidance.

…and 2023 as already a slowdown…despite massive price cuts.

Tesla headed to $100

.

Cultists don’t think so e.g.

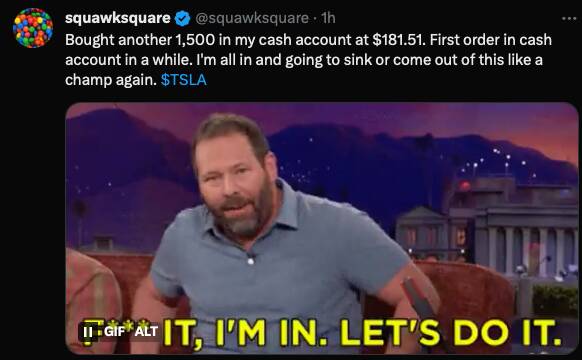

Technically, most likely is $150s, if not then $100. @squawksquare probably betting for a bounce to $230s.

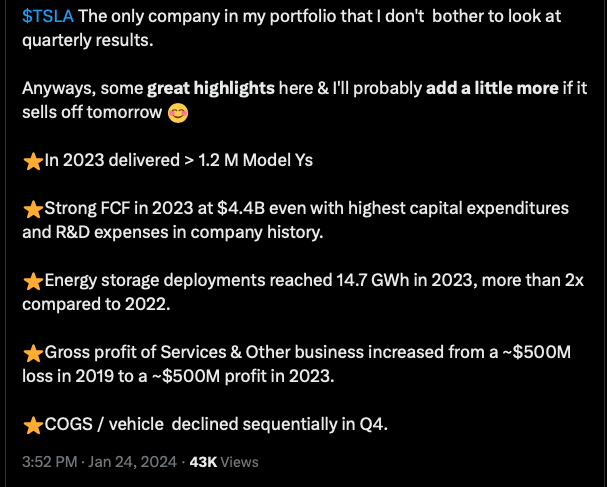

Did he look at quarterly results or not?

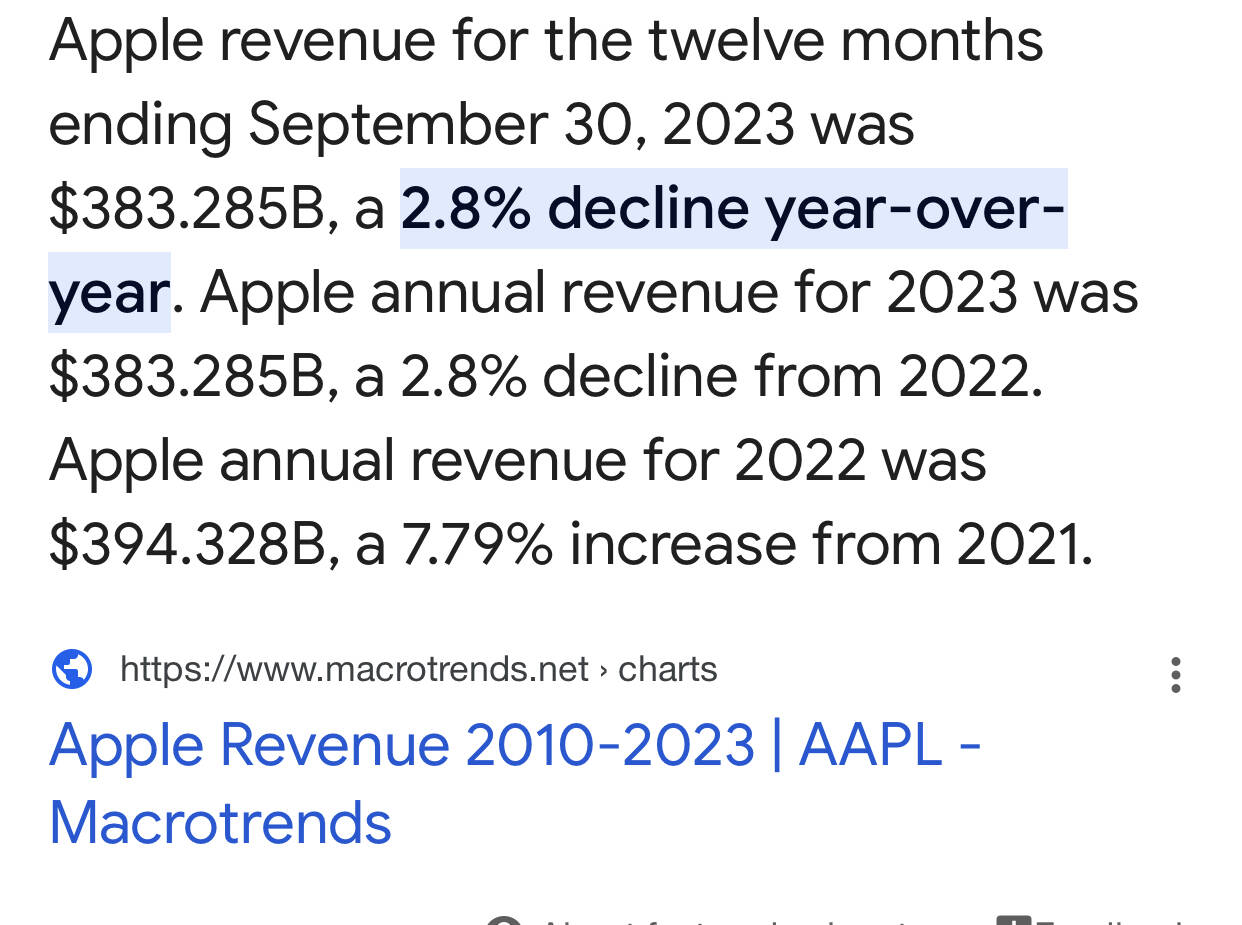

$4.4B free cash flow sounds like a lot to normal people. They are trading at 132x FCF. Meta is 27x. Meta is growing faster. Apple is 30x.

Tesla was brilliant focusing on deliveries over revenue as the key metric. It hides ASP erosion and that unit full-year volumes are growing faster (35%) than actual revenue (15%). Q4 revenue growth was only 3%.

Is anyone excited about a company with 3% revenue growth and 8.2% operating margin?

.

for his bonus.

FIFY ![]()

No wonder you’re so bitter ![]()

I don’t one either. You still own both?