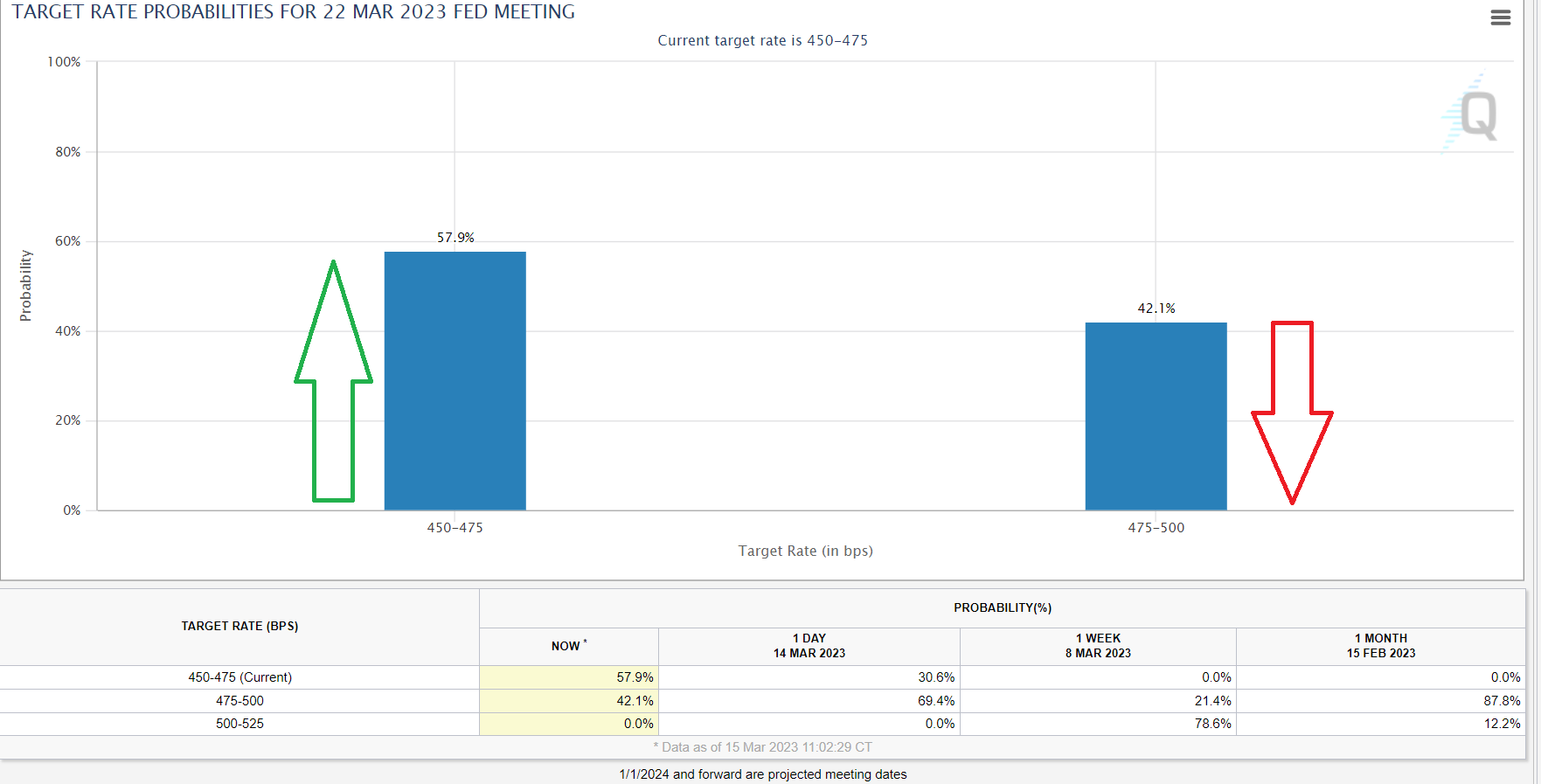

25 basis point 63.5%

No hike 36.5%

50 basis point 0%

Traders are currently pricing in a 63.5% chance the Fed will raise interest rates by a quarter of a percentage point, with 36.5% expecting no increase at the Fed’s March meeting, according to the CME Fed Watch Tool. Traders placed the odds of a half-percentage point rate increase at zero, down from 40.2% just one day ago.

-Unlike 2008, most of the large banks don’t appear to have credit problems from over-aggressive lending, and they are less at risk of liquidity draining from them than small banks. Therefore, most large banks are in decent shape.

-Smaller banks, meanwhile, aren’t out of the woods yet due to the combination of less cash on hand and significant unrealized losses sitting on their balance sheets. The majority of them, at least the publicly-traded ones, don’t have the acute solvency problems that Silicon Valley Bank had, but if they raise deposit rates to try to keep deposits then they do risk experiencing a solvency problem.

-Policymakers will be watching the liquidity situation closely at this point, and are likely to find it difficult to keep moving forward with interest rate increases and quantitative tightening for much longer. Specifically, total U.S. bank reserves probably can’t go much below the current $3 trillion level without corresponding increases in the usage of liquidity facilities.

-If the Federal Reserve is unable to keep up the combination of interest rate increases and quantitative tightening for much longer due to hurting small banks too much, despite price inflation still being above-target, then a basket of anti-dollar positions such as gold, oil, commodities, emerging markets, and bitcoin would likely benefit.

Imagine if banks have long-dated maturity assets at very low interest rates. Now they have to pay customers higher rates, or they’ll pull their money and go to a different bank. It’s a nightmare scenario if they are paying customers a higher rate than the bond assets are generating.

What happens if inflation stays same @4-5% range average in the next 6 months? Can FED continue this frozen rates position in that case?

ADDED LATER:

Answering my own question:

I guess Fed thinks this interest rate is sufficient(+a small increase for terminal rate) to tamp down inflation. Hope they’re right, they’ve been horribly wrong in the very recent past.

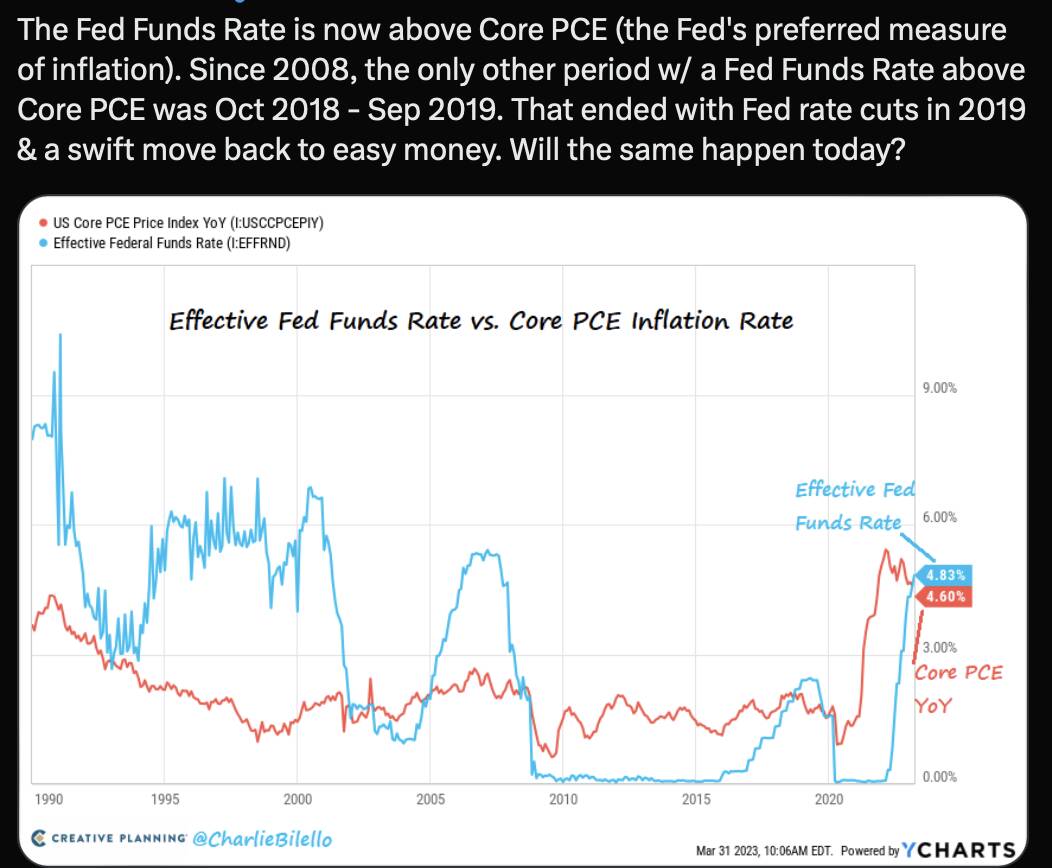

Fed believes so long Fed rate is higher than inflation (I think they use Core PCE), inflation should decline to their targeted 2% (how long, 1-2 years?).

That’s why I equate it to the position formula. Inflation is decreasing which is our velocity. The question is will we maintain that velocity if they stop increasing rates? Also, do they think that’s sufficient velocity? They will rate hike if they feel the velocity is slowing or they want to accelerate it.