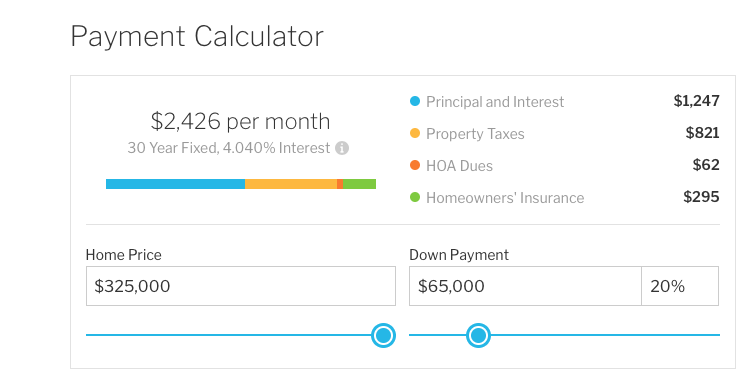

Bought a SFH last year for $325k, rented out at $2250. Assuming a downpayment of 20%, and a mortgage 30 years fixed, 4.04% interest,

Principal & interest $1247

Property Taxes $821

HOA dues $62

Homeowners’ insurance $295 PITI+ HOA = $2426 per month. which is more than monthly rent of $2250.

Renting is cheaper since no need to pay for maintenance & repairs, and asset replacement.

As a landlord, getting 5% cap rate + yearly capital appreciation of 10-15% (not sure what the stable number would be as previous historical figure of 2-3% is obsolete because of tech disruption), is a worthwhile investment. Although is not that great when compare to stock investment, is ok as a diversification.

I paid $345k last year in South Lake Tahoe. House with cottage. Gross rent $3400. 8 cap with expenses… tax about $3600. Insurance $1800, high fire danger area.

Show your number please. I did some computation, not much better. In fact, I run some numbers for a few places in USA, the cap rates seem to be around 4-5%. Not much difference. I think the market self arbitraged.

The post here is not about land lording. Is from the perspective of a renter. According to Harriet, should buy and not rent. But my figures show should rent and not buy. Of course, for us, we tend to look from the perspective of land lord. For me, I don’t look at individual houses or stocks, I think in term of portfolio… quite different

Phoenix property tax is about 1k a year for a 300k house. Actually property tax increase and house market value increases seems to be unrelated. Property tax tracks inflation instead.

Renting is cheaper intheshortrun if appreciation is 0. That explains 90% of USA.

But over longer time horizon, buying is better because

the first letter of PITA is P, the principal. Only interests is expense. Principal money you are paying yourself. As time goes on it will be bigger and bigger part of PITA.

After 30 years you pay off the whole house. Big drop in payment. Rent will never stop.

Frankly too generic for me. Why don’t just randomly select a house and do the figure. I don’t find generic numbers useful. In any case, we are diverting. I just want to look from the perspective of a tenant, why is ok to rent and not try to buy. Not from a land lord.

Btw, hard to believe can get cap rate of 7% from a $300k house charging $2k rent.

If it doesn’t sense to pay $2000 for rent for a house that is worth only $316k, won’t it even more surprising that there are people who is willing to pay higher rent like in South Lake Tahoe, Phoenix and Las Vegas? Can anyone explain why? In Austin, PITI + HOA (+ maintenance & repairs + accrued asset replacement) is higher than rent, so it makes sense that some would rent. But in SLT, Phoenix and LV, it is claimed that PITI + HOA is much less than rent, why would anyone rent?

In Phoenix there are fair number of part-time homes for rent (snow birds own?). Very hard to find homes to rent via airbnb or vrbo Nov-Apr. They charge high. I’m renting a 1200sq house for $205 (incl all the various fees, taxes, etc) per night. All the better homes were all booked up through April.

Places like Florida look good from far but a far from good.

You really need to know the neighborhoods. High caps often mean high expenses and high crime.

I found a gold mine in South Lake Tahoe. Plenty of renters, low inventory, hardly any new construction allowed, its renters are low income with no cash, have to get roommates. They don’t have the option to buy. So most of the competition I have when buying is BA people looking for vacation homes. But they look for turnkey move in ready. I buy fixers that need time and money… Vacation home buyers don’t want to be bothered, don’t have the time… Rents are going up at 10% annually and values too. 6-12 Caps

I did invest in Phoenix, Gilbert actually, large multi family development. We will sell when fully rented.

Have done the same thing in Texas and Florida. Build then sell or fix and flip… in our case projected 28% IRR.

Much better than buying and holding.